By guest contributors Emily Garr Pacetti and Maria Thompson, Federal Reserve Bank of Cleveland

Nonemployer firms—that is, small businesses for which the owner is the only paid employee— represent roughly 81 percent of all small businesses in the United States. These firms can act as a litmus test for an inclusive recovery, helping us either support or refute the idea that credit is getting to the firms that need it most. While not a lot is known about nonemployer firms given the complexity and diversity of individuals they represent (from tech solopreneurs to street vendors to strategy consultants), we know from the Federal Reserve System’s Small Business Credit Survey 2021 Report on Nonemployer Firms that nonemployers are younger, more likely than other small businesses to be owned by immigrants, women, and people of color, and much more likely (70 percent versus 15 percent of employer firms) to have revenues of less than $100k. We also know that their numbers have increased over time. According to the U.S. Census Bureau’s Nonemployer Statistics, there are about 26 million nonemployer firms in the United States, up from about 16 million two decades ago.

The Small Business Credit Survey 2021 Report on Nonemployer Firms is just one of a series of reports from the Small Business Credit Survey (SBCS), a national survey of small businesses conducted by the 12 Federal Reserve Banks. If you are a small-business owner, consider taking the Federal Reserve’s 2021 survey, in the field until November 19.

Here, we explore nonemployer experiences six months into the pandemic, whether these firms received the credit they sought, and what their experiences say about credit challenges that may continue during the pandemic’s second year. We use the Federal Reserve System’s annual SBCS, fielded in fall 2020, to understand the unique credit needs of these smallest of small businesses. (For information on how small employer firms fared as a whole, read the Small Business Credit Survey 2021 Report on Employer Firms and EIG’s latest “Taking the Pulse” update on how small businesses are faring, based on the Small Business Pulse Survey.)

Insights from the Survey Data

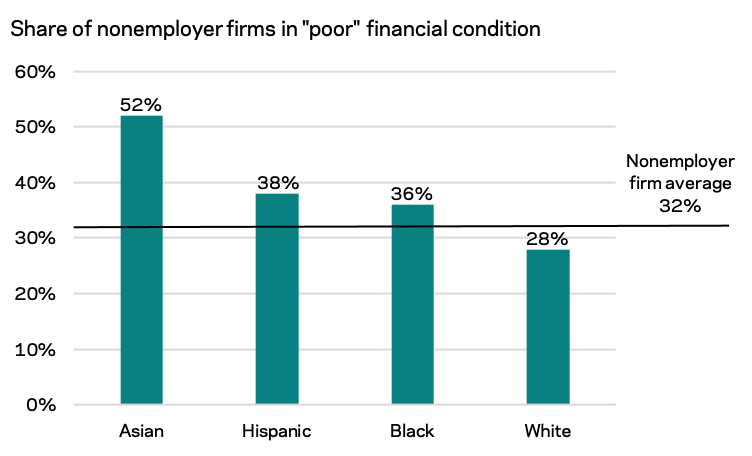

Most small businesses, both employers and nonemployers, were in a precarious position early in the pandemic: about 80 percent reported financial challenges in the 12 months leading up to the fall 2020 survey. Among nonemployers specifically, 32 percent described their financial condition as “poor” six months into the pandemic, with the share highest for Asian-owned firms (52 percent) and lowest for white-owned nonemployers (28 percent). A majority of nonemployers reported that the firm was the primary source of income for their household, and upwards of 80 percent reported an impact on their personal finances due to pandemic-related challenges.

Source: Federal Reserve System, Small Business Credit Survey 2021 Report on Nonemployer Firms

Given these vulnerabilities, did nonemployer firms get the help they needed? Unfortunately, no. Nonemployers were both less likely than employer firms to seek emergency funding and less likely to be approved when they did. This was true regardless of the race or ethnicity of the owner. COVID-19-related assistance included a range of new funding sources, such as the Paycheck Protection Program (PPP) and the COVID-19 Economic Injury Disaster Loan, or EIDL, program (EIDL applications are open through December), designed to help small businesses stay afloat. Although PPP and EIDL were fairly evenly accessed by nonemployers (35 and 37 percent of nonemployers applied to the loan programs, respectively and 29 percent for EIDL grants), 19 percent did not seek assistance to any program even though they reported a need for funds. Additionally, about 30 percent of nonemployer firms reported collecting unemployment insurance, made possible through the CARES Act which expanded eligibility to independent contractors and other self-employed workers.

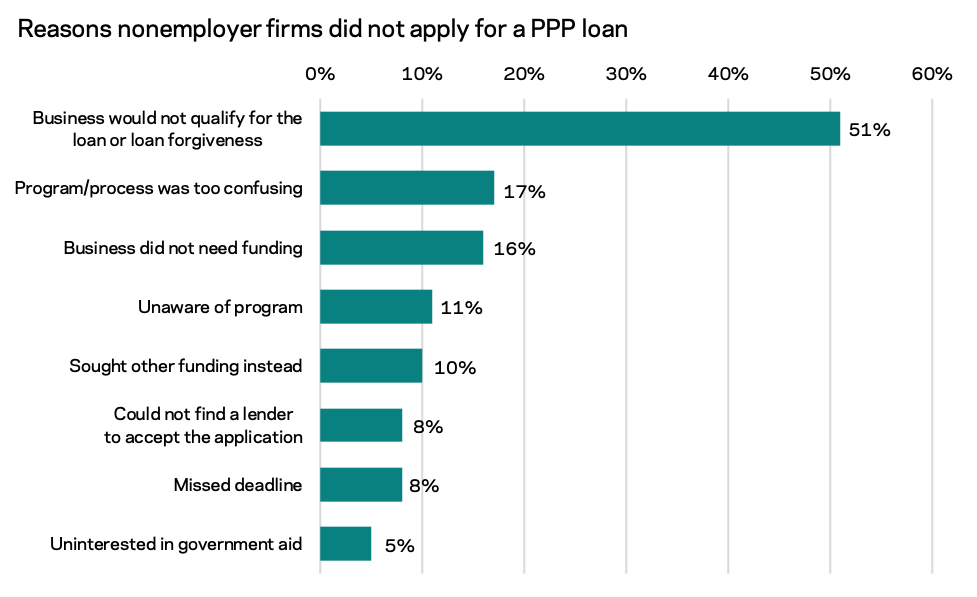

Many nonemployers reported uncertainty about the different programs and eligibility requirements, or they lacked banking relationships necessary to secure funding. For the PPP specifically, 57 percent of nonemployer firms received the full funding amount they sought, compared to 77 percent of employer firms. Of the 65 percent of nonemployers who did not apply for the PPP, the most cited reasons were that the owner expected that the “business would not qualify for a loan or for loan forgiveness” and “the program/process was too confusing.”

Source: Federal Reserve System, Small Business Credit Survey 2021 Report on Nonemployer Firms

Elizabeth McGinsky of the Enterprise Center in Philadelphia shared that “due to opaque communications about the rules for collecting unemployment and PPP assistance, our nonemployer firms typically weren’t in a position to access either [for fear of] future bills or tax liabilities…or, in the case of unemployment, they may not have been able to navigate unemployment red tape at the state level.” Jeff Wicklund, also of the Enterprise Center, noted that “Wording like the ‘paycheck protection program’ made it sound like the program was for employer establishments, so our nonemployer businesses did not realize they were eligible even after rules changed to expand eligibility.”

The experience of the staff at the Enterprise Center, which served more than 1,200 small businesses mostly in Pennsylvania and New Jersey in 2020—a 50 percent increase from 2019—suggests that communications and information was in fact just as much as a barrier as program eligibility and credit availability. And Enterprise Center’s experiences were not unique.

Frustration Leads to Solutions

Such perspectives of nonprofit leaders, particularly in older industrial places, shed light on the complexity and diversity of nonemployers and the challenges that even the most resilient businesses and most robust small business ecosystems face. Over the past year, Federal Reserve Banks hosted critical conversations with small businesses and local and national intermediaries that brought to light the range of business needs in the pandemic. The conversations underscored the difficulty this sector had accessing credit given the lack of support structures and established banking relationships. It was there we heard that customized, community-based outreach through trusted intermediaries proved a gamechanger for nonemployers seeking credit—an important lesson for any future efforts. Examples include Neighborhood Allies in Pittsburgh, Pennsylvania, that brokered banking relationships with disadvantaged firms; MidTown Cleveland in Cleveland, Ohio, whose director of AsiaTown initiatives noted the importance of language translation; and many other testimonies from across the nation that emphasized the importance of networks and collaboration when filling information gaps.

Fortunately, stories like those shared above prompted programmatic and policy changes intended to increase access for small businesses in greatest need. For example, in March 2021, the PPP began clearly distinguishing loan amounts for sole proprietors both with and without payroll costs. And translation to multiple languages is readily available on the PPP and EIDL sites today.

Towards Inclusion of All Small Businesses — Why Data Matter

Part of the reason why programs may not be well targeted to many nonemployers may be that policy makers simply do not know enough about them. The SBCS gives us critical information that can be used to better inform and shape more effective policies that can respond to this diverse bedrock of small businesses. We know from the SBCS that 94 percent of nonemployers anticipated pandemic-related challenges in the 12 months following the fall 2020 survey, yet one-quarter of nonemployers still planned to add employees. The 2021 survey will offer insight into what became of those predictions, and whether policy and programs rose to meet the need of some 26 million firms across the country.

The 2021 Survey is in the field now and—with sufficient survey responses—we can ensure that the experiences of all small businesses, particularly the smallest and most vulnerable, are documented, debated, and applied long after the worst of the pandemic is behind us.

If you’re a for-profit, small-business owner with 0 to 500 employees, the Federal Reserve System invites you to take the 2021 Survey before November 19, 2021.

To learn more about the SBCS, visit https://www.fedsmallbusiness.org/survey.

Related:

Small Business Credit Survey 2021 Report on Nonemployer Firms

Small Business Credit Survey 2021 Report on Employer Firms

Small Business Credit Survey 2021 Report on Firms Owned by People of Color

How Well Did PPP Loans Reach Low- and Moderate-Income Communities?

Equality Is Not Enough: Reflections on the Paycheck Protection Program

Struggle for Access: Small Lenders, Small Businesses, and the Paycheck Protection Program