For most of the 21st century, Americans were told we were living

through a period of unprecedented economic change and

transformation. Record waves of startups and new technologies

were unleashing disruption across the economy. Headlines blared

about gig work and automation turning the labor market upside

down. So dizzying was the pace of change that we would need to

reimagine the future of work, the social contract, and even

capitalism itself. Reflecting the consensus, one prominent

senator declared that we were in the midst of “arguably the

largest economic disruption in recorded human history.”

But none of these claims was actually true. Instead, America was

mired in a period of unprecedented complacency. The very thing

that people were told to fear–rapid change and progress–had gone

inexplicably missing.

In fact, American dynamism was in a decades-long retreat.

Startup rates languished near all-time lows. Fewer companies

were going public. Corporate America looked old and complacent.

Increasingly, too, did American demography. U.S. productivity

growth dramatically decelerated in spite of promising new

technologies. And a country whose people were once known for

their restless, pioneering spirit became increasingly stuck in

place.

Simply put: America was losing its mojo.

But now, after a prolonged period of relative stasis, the

pandemic has jolted key indicators of economic dynamism–at least

temporarily–back to life. The labor market is churning as job

quits matched their highest levels on record in November 2021,

when 3 percent of the workforce quit in a single month. IPOs are

back to levels last seen in the heyday of the technology boom in

the late 1990s and early 2000s. Firms are pouring resources into

new technologies, developing new processes, and embracing new

work arrangements with their employees. And entrepreneurship

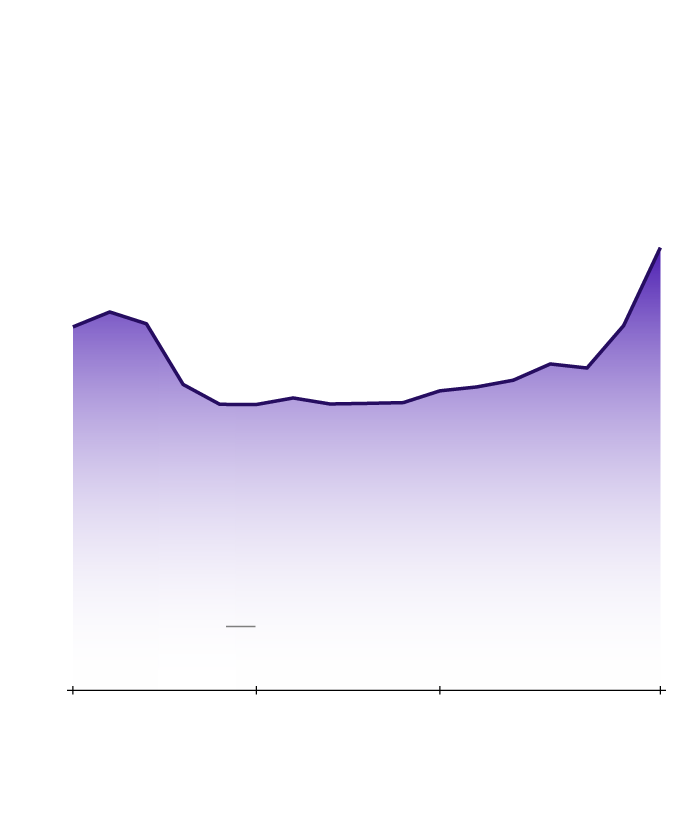

appears to be surging: in 2021, a record 1.8 million

applications were filed to start new “likely employer”

enterprises–37 percent more than in 2019.

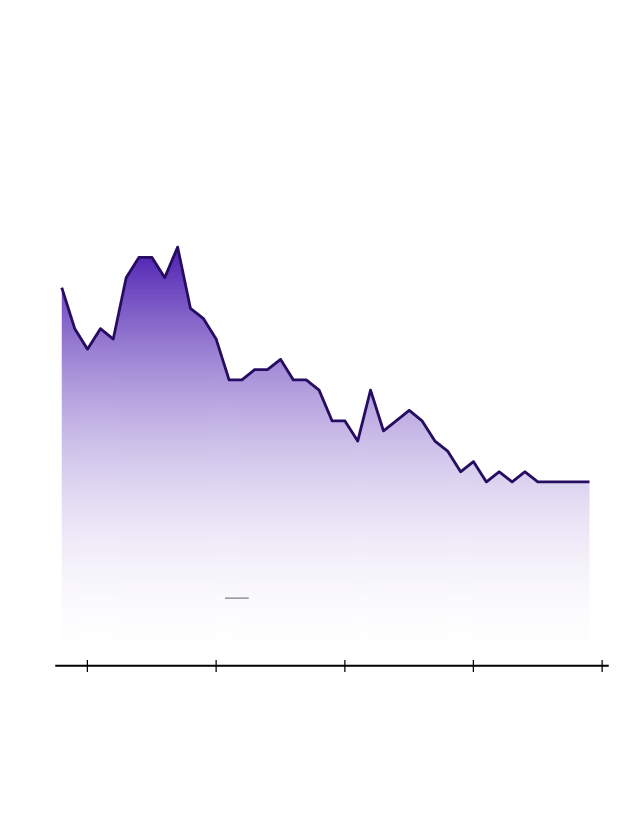

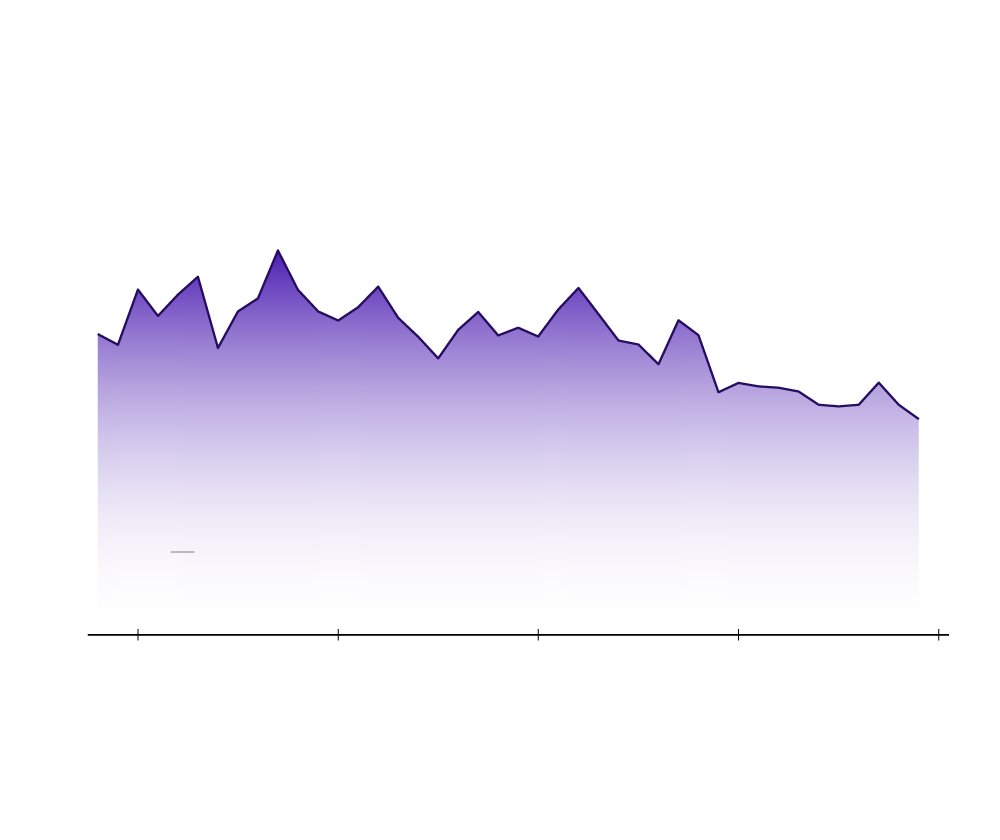

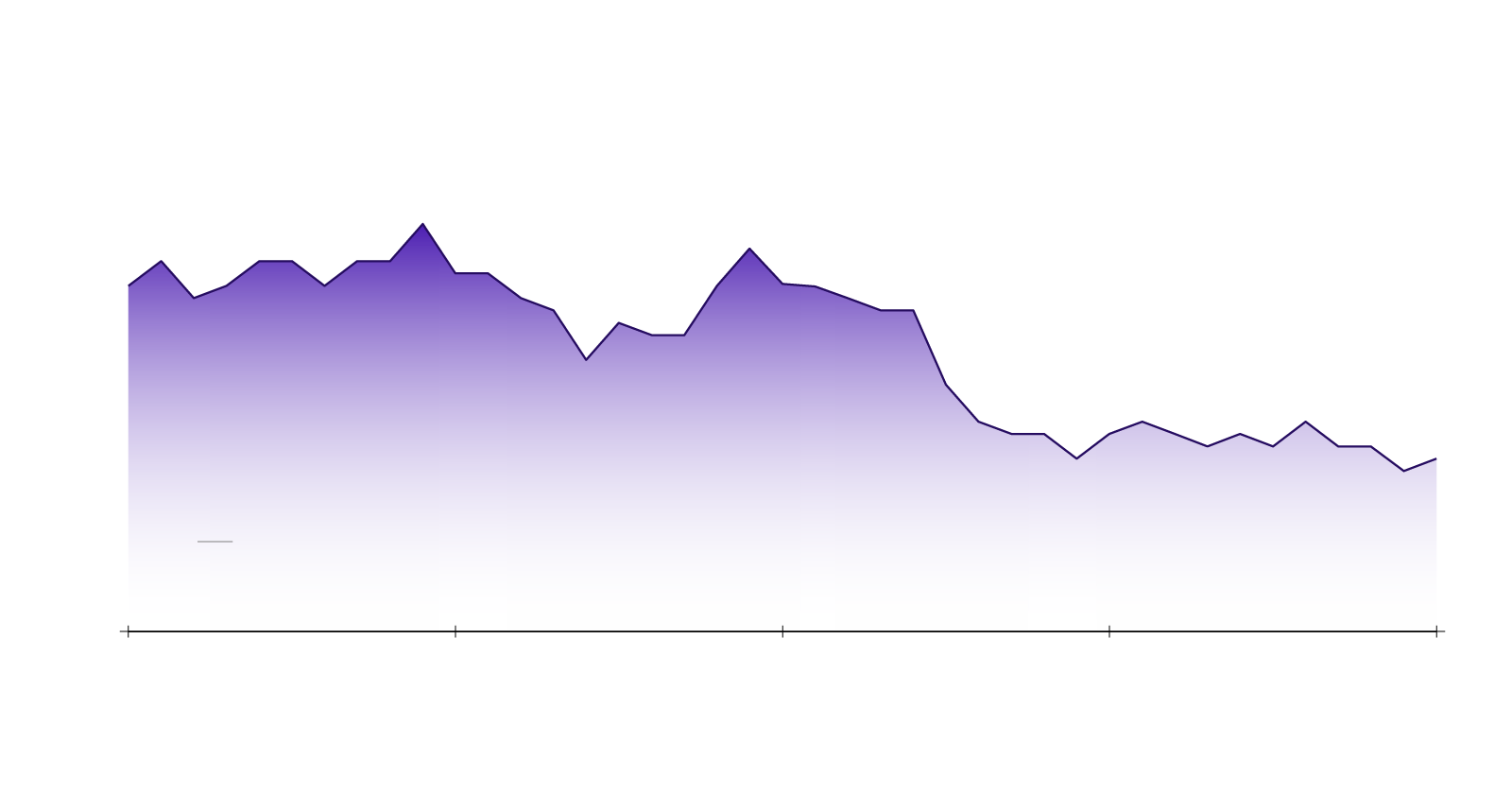

In 2021, the pandemic helped spur the

largest number of new likely employer

business applications on record

Annual total of likely employer

business applications (millions)

1.8

1.5

1.0

0.5

Recession

periods

0.0

2005

2010

2015

2021

Source: U.S. Census Bureau’s Business Formation

Statistics

In 2021, the pandemic helped spur the largest number

of new likely employer business applications on record

Annual total of likely employer business applications

(millions)

1.8

1.5

1.0

0.5

Recession

periods

0.0

2005

2010

2015

2021

Source: U.S. Census Bureau’s Business Formation

Statistics

In 2021, the pandemic helped spur the largest number

of new likely employer business applications on record

1.8

Annual total of likely employer business applications

(millions)

1.5

1.0

0.5

Recession

periods

0.0

2005

2010

2015

2021

Source: U.S. Census Bureau’s Business Formation

Statistics

Look beyond the current momentum, however, and it remains clear

that powerful headwinds are working against a return to the

high-churn qualities that once characterized our economy. While

the quantity of new businesses in the pipeline appears

record-breaking, questions remain about their quality and

longevity. The pandemic has accelerated the country’s

demographic challenges, pushing population growth and

immigration to historic lows. The continued dominance of

incumbent firms and vested interests across the economy means

that market conditions are not especially hospitable to new

upstarts. The economy is replete with gatekeepers that stymie

workers and slow the pace of adaptation and adjustment. And the

impact of temporary fiscal and monetary stimulus may be

distorting markets and obfuscating the long-term economic

outlook. For the country to overcome these challenges, we must

renew the forces of competition, entrepreneurialism, and

adaptivity that have waned dramatically in recent decades.

In the following paper, we examine the fall and potential

rebirth of American dynamism and why it matters deeply for

American workers. We track the downward trajectory of key

economic indicators, such as startup and job reallocation rates,

and highlight the major forces that help explain their decline.

We reject the notion that Americans must settle for a complacent

future in which stasis and managed decline replace dynamism as

the new norm. We also reject the notion that replacing dynamism

with stasis serves the interests of American workers and

families. Policy mistakes—large and small—compounded over

decades have contributed heavily to the country’s diminished

vitality, but it is not too late to change course. And change is

urgently needed, because a high-churn, dynamic economy is one

that offers the strongest benefits to workers in the form of

abundant jobs and better wages, as well as greater access to

opportunity for marginalized workers. To that end, we conclude

by sketching out the pillars of a pro-dynamism policy agenda

that would unleash the economy’s pent-up potential and help all

Americans share more fully in the benefits of economic growth.

01 Diagnosing the decline

What is dynamism?

The term economic dynamism refers to the rate and

pervasiveness of change across industries, geographies, and

the labor market in an economy.

Key indicators of dynamism traditionally include the rates of

business formation and closure, the frequency at which workers

quit and switch jobs, and the propensity of workers and

families to move to new locations. Economic dynamism is not

simply “disruption”; it equates more closely to a state of

productive churn and adaptation that enables the economy and

its workers to respond to disruption.

Dynamism lies at the heart of a well-functioning market economy.

A robust ferment of churn and change underneath the surface

endows the economy with an inherent flexibility that allows it

to adapt, evolve, and grow. Dynamism is safeguarded by multiple

forces: the intensity of healthy market competition, demographic

vitality, a high-quality human capital base, strong

institutions, and even social and cultural factors like the

population’s entrepreneurial proclivity.

In dynamic economies, firms both form and fail more frequently,

and a healthy startup rate ensures that the economic impacts of

failures are short-lived, as the economy’s natural restorative

forces redeploy workers and resources into new and better

endeavors. Healthy startup rates also ensure that markets remain

competitive, priming a virtuous circle. In dynamic economies,

workers move and change jobs frequently in both pursuit and

attainment of economic opportunity, too. But when dynamism slows

and competition withers, these processes become interrupted, and

imbalances accumulate. Resources go idle. The rate of

experimentation in the economy slows, and it becomes less able

to adapt. Economic opportunities dry up.

The promise of a dynamic economy lies in its ability to ignite

progress and provide insurance against future unknowns.

Dynamic economies generate the innovation and productivity

advances that raise well-being. Constant churn fosters an

underlying resilience that mitigates shocks and smooths

transitions─be they black-swan pandemics or clean energy

revolutions. And dynamism provides its own form of an economic

safety net, with a healthy circulatory system that helps catch

displaced workers and carry them into new occupations and

endeavors.

In short, dynamism helps ensure workers find opportunity in the

midst of economic change.

When the economy’s inherent dynamism begins to ebb, so does its

ability to deliver on the aspirations of American workers and

their families. Unfortunately, that is precisely what has

occurred in recent decades.

Let’s turn now to a closer look at key measures of economic

dynamism and the forces at play behind their steady declines.

The trends

The fall of American entrepreneurship

The startup rate captures the share of all businesses in the

economy that started within the past year, and it may be the

foremost indicator of the economy’s overall dynamism.

Strong startup rates signal a competitive and healthy

marketplace with low barriers to entry that allow new firms to

enter and compete—raising quality, lowering prices, and spurring

further innovation. On the flip side, a healthy firm death or

closure rate is a sign that competitive forces are working:

businesses that are unable to adapt (e.g., improve their goods

and services, offer lower prices, or reduce their production

costs) are forced out of the market, freeing resources to be

deployed more productively elsewhere. In this way, firm births

and deaths go hand in hand, as the flow of new entrants into a

market puts healthy pressure on incumbents, some of whom will

rise to the challenge of increased competition, while others

perish. Healthy startup rates help mitigate the tangible

downsides of firm closures for workers by ensuring they can

quickly find employment elsewhere. Without a steady flow of new

firms, workers feel the pain of each closure more acutely.

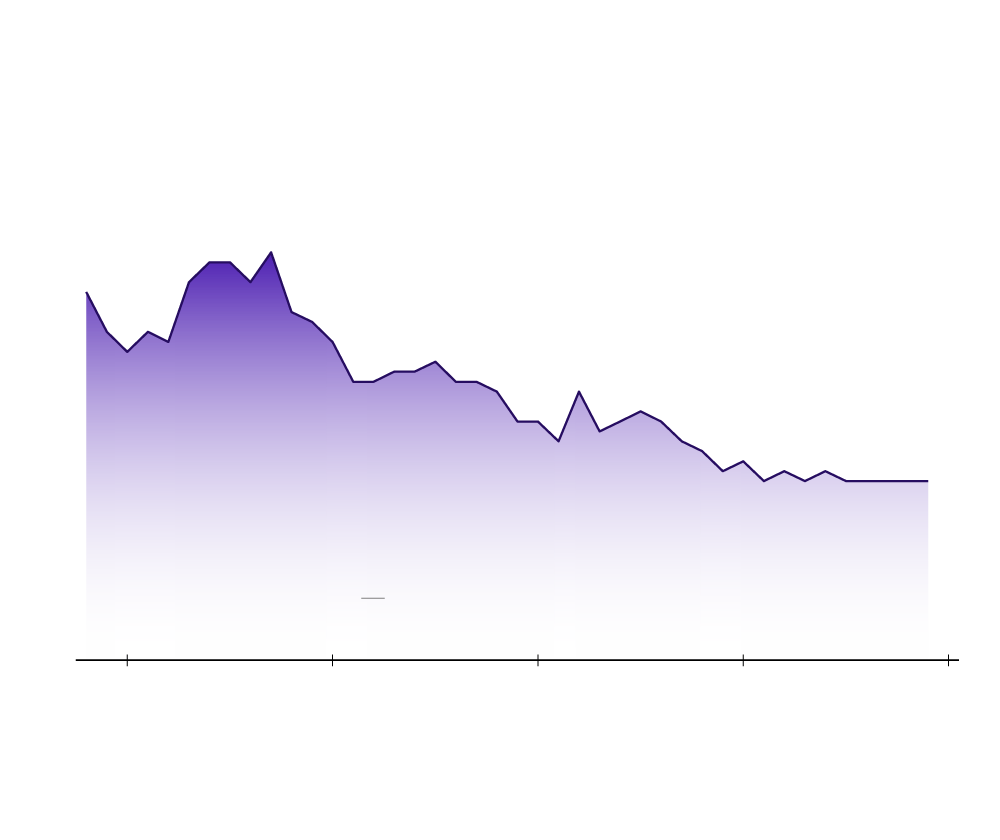

The business

startup rate has

languished near its all-time low point

for over a decade

U.S. startup rate and firm death rate

12%

Startup rate

8%

Firm death rate

4%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The business

startup rate has

languished

near its all-time low point for over a decade

U.S. startup rate and firm death rate

The startup rate

plummeted between

2006 and 2010...

12%

8%

Firm death rate

... from then until the

coronavirus pandemic,

it hardly budged from

its record low

4%

Recession

periods

0%

1980

1985

1990

1995

2000

2005

2010

2015

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The business

startup rate has

languished near its

all-time low point for over a decade

U.S. startup rate and firm death rate

The startup rate

plummeted between

2006 and 2010...

12%

8%

Firm death rate

... from then until the

coronavirus pandemic,

it hardly budged from

its record low

4%

Recession

periods

0%

1980

1985

1990

1995

2000

2005

2010

2015

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The startup rate has been trending downwards since the 1980s,

but two pivotal points stand out in the data. The first occurred

around the year 2000, when startup rates and the incidence of

high-growth young firms in high-tech industries fell sharply for

a decade. The late-2000s financial crisis then brought another,

more wide-reaching watershed. The startup rate plummeted across

sectors and geographic regions between 2006 and 2010. From then

until the onset of the coronavirus pandemic, it hardly budged

from its record low. The rate at which firms die also slowed

around the same time, albeit to a lesser extent. The result was

a low-dynamism equilibrium that lasted for the duration of the

2010s in which firm starts barely exceeded firm closures at the

national level—and actually fell below in many metropolitan and

rural areas. No longer did the American economy comfortably add

new firms at a faster pace than old ones that went out of

business.

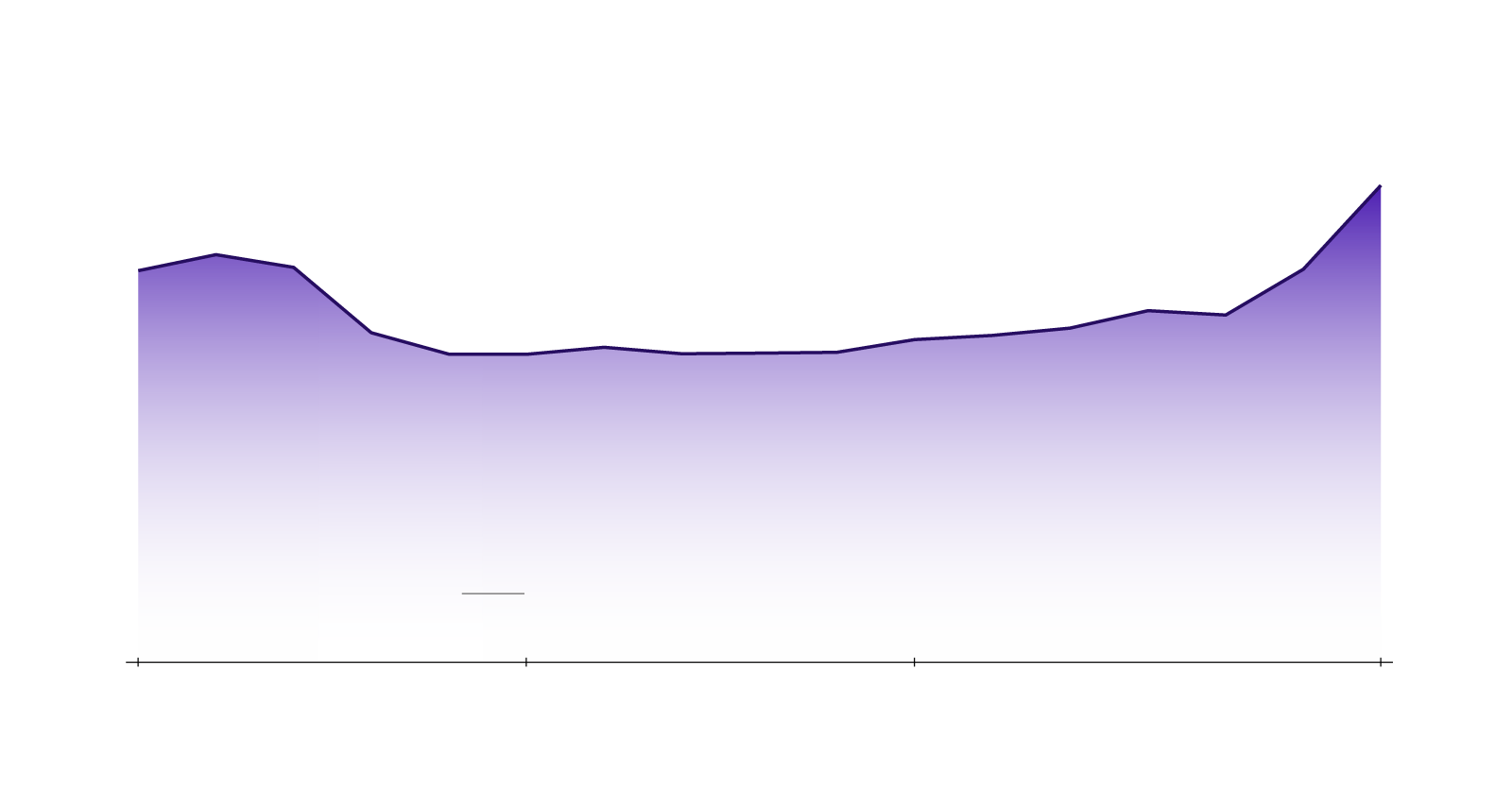

Nowhere is the fading heft of startups more apparent than in

employment data. In the mid-1980s, roughly 4 percent of the

workforce was employed in a company that started within the past

year. By 2010, the figure fell below 2 percent, where it

remained through 2019. In absolute terms, startups launched in

2019 employed 2.4 million workers—the same number as were

employed by new firms in 1982, when the workforce was 57 million

workers (or 43 percent) smaller. Two core factors contribute to

startups’ diminished weight in labor market: startups are both

smaller (the average startup now has only four employees at

founding, compared to five in the 1990s) and scarcer (the

country produced almost 10 percent fewer new firms in absolute

terms in the late 2010s than it did in the 1990s or early 2000s)

than they used to be.

The share of Americans employed

in startups has fallen by one-half

since the mid-1980s

Share of total employment in startups

4%

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The share of Americans employed in startups has fallen

by one-half since the mid-1980s

Share of total employment in startups

4%

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The share of Americans employed in startups has fallen

by one-half since the mid-1980s

Share of total employment in startups

4%

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The graying of corporate America

The flip side of declining startups is the increasing dominance

of older incumbent firms. The share of workers employed in older

firms (defined here as firms that have been in business for at

least 16 years, based on age groups provided by the Census

Bureau) has steadily risen since the turn of the 21st century,

reaching 74.9 percent in 2019. This trend is broad-based across

industry sectors; between 2000 and 2019, only the mining,

quarrying, and oil and gas extraction sector saw its share of

employment in older firms decline meaningfully. The comparative

youthfulness of the extraction industries can likely be

explained by the technological revolution in hydraulic

fracturing – a textbook case in how dynamism within sectors can

transform industries, create wealth, increase productivity, and

reshape economic geography.

Nearly every industry now has

a larger share of workers in

old firms

than at the start of the century

Percentage-point differences in share of

employment in firms aged 16 or older

between 2000 and

2019, by sector

Admin, Support,

Waste Mgmt, Rem. Serv.

+23 pp

Wholesale Trade

+17 pp

Professional, Scientific, and

Technical Services

+17 pp

Construction

+16 pp

Arts, Entertainment, and Recreation

+15 pp

Accommodation and Food Services

+15 pp

Real Estate and Rental and Leasing

+12 pp

Health Care and Social Assistance

+12 pp

Manufacturing

+11 pp

Retail Trade

+10 pp

Information

+9 pp

Management of Companies

and Enterprises

+9 pp

Transportation and Warehousing

+9 pp

Other Services (except Public

Administration)

+7 pp

Finance and Insurance

+6 pp

Utilities

+2 pp

Educational Services

-1 pp

Mining, Quarrying, and Oil and

Gas Extraction

-10 pp

Source: U.S. Census Bureau’s Business Dynamics

Statistics

Nearly every industry now has a larger share of

workers in old firms than

at the start of the century

Share of employment in firms aged 16 or older by sector

0%

20%

40%

60%

80%

100%

2000

2019

Utilities

Management of Companies and Enterprises

Manufacturing

Finance and Insurance

Retail Trade

Wholesale Trade

Transportation and Warehousing

Educational Services

Information

Health Care and Social Assistance

Admin, Support, Waste Mgmt, Rem. Serv.

Other Services (except Public Administration)

Arts, Entertainment, and Recreation

Professional, Scientific, and Technical Services

Mining, Quarrying, and Oil and Gas Extraction

Real Estate and Rental and Leasing

Construction

Accommodation and Food Services

Source: U.S. Census Bureau’s Business Dynamics

Statistics

Nearly every industry now has a larger share of workers

in

old firms than at the

start of the century

Share of employment in firms aged 16 or older by sector

0%

20%

40%

60%

80%

100%

2000

2019

Utilities

Management of Companies and Enterprises

Manufacturing

Finance and Insurance

Retail Trade

Wholesale Trade

Transportation and Warehousing

Educational Services

Information

Health Care and Social Assistance

Admin, Support, Waste Mgmt, Rem. Serv.

Other Services (except Public Administration)

Arts, Entertainment, and Recreation

Professional, Scientific, and Technical Services

Mining, Quarrying, and Oil and Gas Extraction

Real Estate and Rental and Leasing

Construction

Accommodation and Food Services

Source: U.S. Census Bureau’s Business Dynamics

Statistics

As a rule, old firms are slower growing than young firms, if

they grow at all. Thus, the shift in economic weight towards

older (and often larger) firms leaves the economy less dynamic

overall and more dependent on a dwindling cohort of new and

younger firms to power job growth.

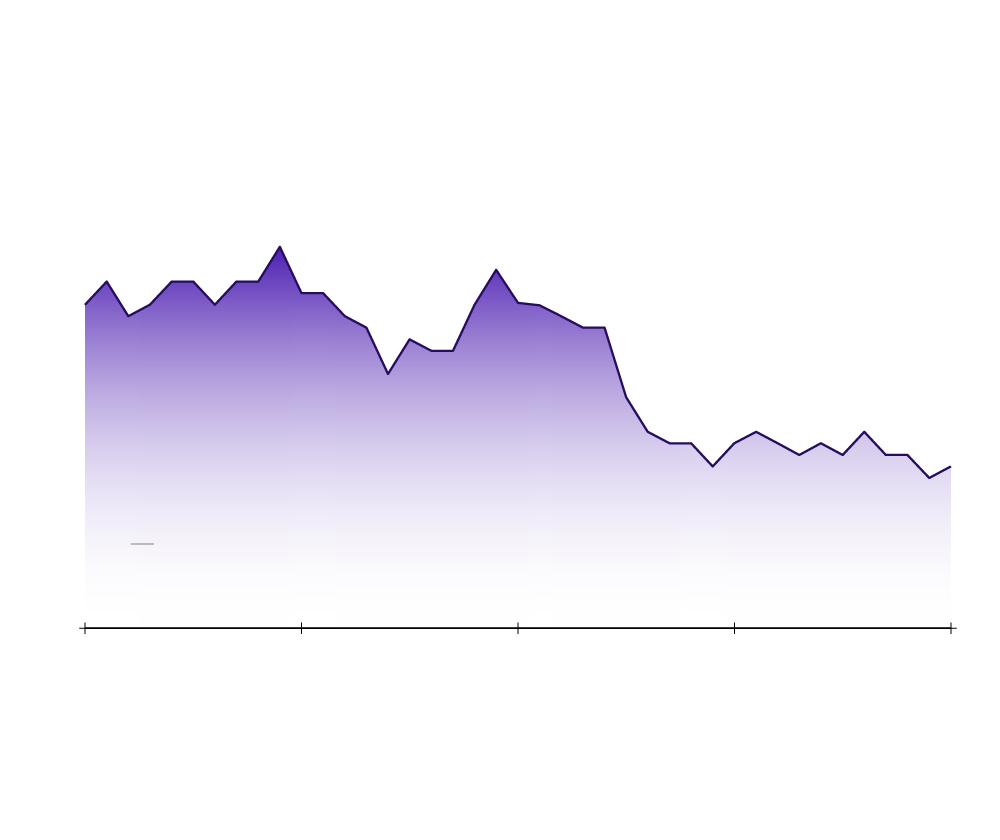

The slowing churn of workers in the labor market

Contrary to popular myths regarding today’s job-hopping

millennials and gig economy precariat, churn in the American

labor market has actually dampened over time. Even the record

number of job quits registered in late 2021 only pushed total

hires and separations in the economy (workforce turnover) back

to levels last seen around 2000. For the duration of the

recovery from the Great Recession, turnover rates for prime-age

workers failed to recover to pre-crisis levels.

The stagnation appears even more acute when examining the net

volume of jobs created and destroyed across firms (job

reallocation) in the economy.

Job reallocation versus workforce turnover: What’s the

difference?

These two terms refer to distinct but complementary concepts.

Job reallocation is assessed at the firm level and offers an

aggregate measure of how the distribution of jobs or positions

in the economy shifts across firms each year. The reallocation

rate is driven by new firm starts, firm closures, and the

differential rates of expansion and contraction of different

businesses. Workforce turnover, by contrast, refers to the

rate at which workers change employers. A job position does

not need to be reallocated between two firms for workers to

turnover among them, for example. Job reallocation is

important for aggregate economic productivity, while workforce

turnover is important for an individual’s career and wage

growth, along with promoting quality job matches.

In the 1990s, the equivalent of roughly one-quarter of all jobs

in the economy were reallocated across companies annually as

firms expanded, contracted, started, and failed in any given

year. By the 2010s, that figure hovered around one-fifth—a 20

percent decline. In 2019, job reallocation reached an all-time

low. While it may sound arcane, job reallocation is an integral

economic process; its slowdown reflects a broader falloff in the

rate at which even successful firms scale and grow. Economists

Ryan Decker and colleagues calculate that falling job

reallocation drove aggregate productivity growth more than

one-third lower in the 2000s than it otherwise would have been.

And of course, the situation deteriorated further over the

2010s.

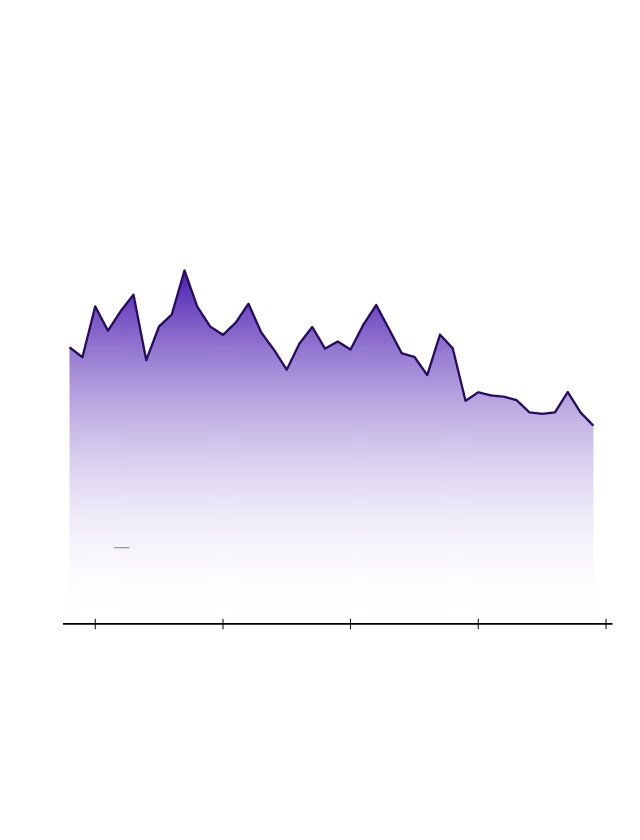

The rate at which workers churn

across firms slowed to its

lowest level on record in 2019

Job reallocation rate

30%

20%

10%

Recession

periods

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The rate at which workers churn across firms slowed

to its lowest level on record in 2019

Job reallocation rate

30%

20%

10%

Recession

periods

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The rate at which workers churn across firms slowed

to its lowest level on record in 2019

Job reallocation rate

30%

20%

10%

Recession

periods

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Business Dynamics

Statistics

The falling job reallocation rate is an important corollary to

the other patterns discussed here: fading startup rates,

disappearing cohorts of high-growth young firms, and an aging

firm distribution. While the slowdown in worker turnover may

partially be attributable to improved employer-employee matches,

the broader decline in job reallocation has negative aggregate

economic implications, given the important role the process

plays in helping to ensure that American workers are employed

productively and paid well in return. The weak startup and

worker reallocation rates coming out of the Great Recession

explains some of the slow productivity and weak wage growth of

the 2010s.

Stuck in place

Once a restless bunch, Americans have become more firmly stuck

in place over the past two decades than at any period on record.

Interstate mobility (i.e., moving across state lines) has

historically served as an important mechanism for reducing

economic disparities across the country, allowing workers to

leave struggling places in pursuit of better economic

opportunities elsewhere. However, interstate migration has

fallen by half since the 1980s, with much of that decline coming

in the immediate run-up to the Great Recession. The interstate

migration rate hit a record low in 2019, as Bill Frey from the

Brookings Institution has chronicled.

Americans have never been

less likely to move across state lines

Interstate migration within U.S. population

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Historical Migration

and Geographic Mobility Tables

Americans have never been

less likely to move across state lines

Interstate migration within U.S. population

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Historical Migration

and Geographic Mobility Tables

Americans have never been less likely to move across

state lines

Interstate migration within U.S. population

3%

2%

1%

Recession

periods

0%

1980

1990

2000

2010

2020

Source: U.S. Census Bureau’s Historical Migration

and Geographic Mobility Tables

Meanwhile, migration has become increasingly skill-biased, with

highly educated Americans moving at much higher rates compared

to those who only have a high school diploma. Several factors

likely contribute to the decline in mobility, and a perceived

reduction in economic opportunities elsewhere appears to be a

significant one: between 2000 and 2010, more than half of the

decline in residential migration was the result of declines in

economic migration (i.e., moving because of a job change).

Contrary to initial expectations, the pandemic has delivered no

observable reversal to this trend. Whether down the street,

across town, or across the country, Americans moved less during

the pandemic than any time on record. None of this is to say

that Americans are satisfied with declining geographic mobility.

The share of Americans who report being stuck in a neighborhood

they would like to leave has risen by nearly 50 percent over the

past four decades.

The forces at work

What explains America’s lost mojo? The decline in U.S. dynamism

is widespread across sectors and regions of the country, and is

mirrored across advanced economies around the globe. This

pervasiveness suggests that several different and interrelated

forces operating on economy-wide scales are likely behind the

development. Disentangling them is difficult, but economists

generally see two basic causes: slowing rates of population

growth and slowing rates of knowledge diffusion. We would add a

third: the generalized, all-encompassing shift towards

gatekeeping at every level of economic life, which makes it

harder to build, move, switch jobs, start firms, and compete.

Demography

A young and growing population helped buoy the U.S. economy for

most of the 20th century with plentiful labor and a growing

consumer base. No longer. The 2010s were the second-slowest

decade for population growth in the country’s entire history,

barely beating out the 1930s, which included the Great

Depression and strong restrictions in immigration policy.

Between 2010 and 2019, 81 percent of counties saw their prime

working-age population (i.e., 25- to 54-year-olds) decline (see

Figure 10). The share of the country’s labor force in their

prime entrepreneurship years fell by 7 percentage points from

2000 to 2019. The pandemic pushed annual population growth to

0.1 percent in 2021–the lowest in the country’s history.

This slowdown has many implications, both for labor market

outcomes and the broader economy. A declining population means

fewer workers and fewer consumers to stimulate economic

growth—as well as fewer would-be entrepreneurs. Work by Ian

Hathaway and Bob Litan has shown that population growth is a

strong contributor to new business formation. Fatih Karahan and

colleagues estimate that the slowdown in labor force growth

since 1970 may account for 33 percent to 60 percent of the

decline in the startup rate. It may also help explain why the

startup rate has remained stuck at historically low levels

despite the return to broader macroeconomic growth. Even at the

county level, population growth is associated with higher

startup rates, while a 1 percent loss in population leads to a 2

to 3 percent decline in the local startup rate. With national

population growth so slow and localized population losses so

widespread, demographically induced dynamism can no longer be

taken for granted.

The country’s population

grew more slowly during the

2010s than

at any point since the Great Depression

U.S. population growth rates by decade

20%

15%

10%

5%

0%

1900s

'20s

'40s

'60s

'80s

2000s

Frey. “For the First Time on Record, Fewer than

10%

of Americans Moved in a Year.” Brookings

Institution, 2019

The country’s population grew more slowly during

the 2010s than at any

point since the Great Depression

U.S. population growth rates by decade

20%

15%

10%

5%

0%

1900s

'10s

'20s

'30s

'40s

'50s

'60s

'70s

'80s

'90s

2000s

'10s

Frey. “For the First Time on Record, Fewer than

10% of Americans Moved in a Year.”

Brookings Institution, 2019

The country’s population grew more slowly during

the 2010s

than at any point since the Great Depression

U.S. population growth rates by decade

20%

15%

10%

5%

0%

1900s

'10s

'20s

'30s

'40s

'50s

'60s

'70s

'80s

'90s

2000s

'10s

Frey. “For the First Time on Record, Fewer than

10% of Americans Moved in a Year.” Brookings

Institution, 2019

Knowledge diffusion

The spread of knowledge and expertise is key to an economy’s

dynamism. While there are inherent measurement challenges at

play, a growing body of evidence points to the decline in the

rate at which knowledge diffuses through the economy as a

cause—not just a consequence—of declining American dynamism.

This decline may seem paradoxical in the age of information

technology, but economists estimate that diminished knowledge

diffusion accounts for up to 70 percent of the observed symptoms

of diminished dynamism, from high corporate markups to slowing

startup rates and aborted growth trajectories of young firms.

Recent research from the Organization for Economic Cooperation

and Development (OECD) finds that dynamism’s decline has been

swiftest in the most digitized and knowledge-centric advanced

economies.

Obstructions to the flow of knowledge would be consistent with

observations by Ryan Decker and colleagues that high-growth,

high-wage startups have disappeared even more quickly than other

types of startups. Why might these critical economic

inputs—knowledge and ideas—not be flowing as freely as they used

to? The answer may be wrapped up in the nexus between technology

and market concentration. Digitization offers leading companies

compounding advantages that extend their lead and entrench their

dominance, making it harder for upstarts and laggards alike to

compete. Indeed, further evidence from OECD economists suggests

that the hold that superstar firms have over new knowledge is

tighter and longer lasting than ever before. Overlapping

thickets of patents perpetuate the gaps and slow the rate at

which new technologies get absorbed by other firms and deployed

across the economy. Strategic acquisitions are used to either

snuff out would-be competitors or seize innovations to further

strengthen incumbent advantage.

Startups play a critical economic role in commercializing

innovations, which means their retreat could be a symptom of

slowing innovative activity further upstream as well. Falling

federal investment in basic R&D—the earliest-stage fountain of

new knowledge and where the public sector has the greatest

comparative advantage—relative to the size of the economy (or

the waning effectiveness of such spending) could be making

itself felt in less new knowledge and technology flowing

throughout the system, for example, and fewer new business

opportunities as a result. To be sure, on many measures the

country still produces large crops of extremely innovative, high

quality new firms in most years, but the volume, variety,

survival, and growth of such firms lags far behind the economy’s

potential—and its history.

Workers themselves are essential in spreading knowledge and

know-how throughout the economy but face mounting barriers at

every turn. The proliferation of restrictive employment

covenants such as non-compete agreements prevent knowledge

workers from moving to competitors or starting their own firms.

Frivolous lawsuits and opportunistic trade secret enforcement

actions undermine risk-taking in our most innovative sectors.

Fewer spin-offs, fewer job-hops, and fewer cross-country moves

all bolster the sequestration of knowledge behind moats of

intellectual property and other protections that advantage the

goliaths. All of this slows the pace that know-how and

innovations filter through the economy, and it translates into

fewer opportunities to start and scale new businesses around new

ideas.

Sclerosis

In 1982, economist Mancur Olson coined the term “institutional

sclerosis” to describe the process through which rich, stable

democracies become weighed down with vested interests,

bureaucratic overreach, and forms of inefficiency and

gatekeeping over time. This sclerosis makes economies slower and

less flexible, eventually sapping market-based democratic

systems of much of their strength and reducing productivity,

growth, and individual economic mobility. One can easily see

this diagnosis applying to the United States today, where

mojo-destroying inaction and stasis define so many aspects of

economic life.

Perhaps nowhere is the sclerotic build-up more apparent than in

sectors touching the built environment itself. The American

construction industry has experienced almost no productivity

gains in multiple generations. It costs more to build new

transportation infrastructure in the United States than nearly

anywhere in the developed world. This chokes off the economic

potential of major infrastructure investments. It suggests that

absent a broader institutional cleanup, even major federal

efforts to modernize and expand the country’s infrastructure are

at risk of getting stuck in a morass of permitting delays and

cost overruns—and ultimately underdelivering for the American

people. As Brink Lindsey of the Niskanen Center warns, “a

government that cannot build things on time and on budget is a

government incapable of providing the public goods the 21st

Century demands.” Indeed, our inability to build to meet even

our most exigent priorities threatens the nation’s ability to

successfully transition to a lower carbon economy.

At the federal level, the mass of rulemaking appears only to

grow. Declining dynamism writ large cannot be pinned on the

growing volume of federal regulation alone, but complexity is a

gift to large incumbents and vested interests all the same. What

happened to the country’s banking sector in the wake of the

2008-09 financial crisis is telling. As tomes of new financial

rulemaking were spun in the wake of the crisis, entrepreneurship

in the country’s traditional banking sector was completely

neutralized for nearly a decade. More than 1,500 new banks were

chartered in the 10 years prior to the financial crisis; between

2011 and 2018, only 14 were. Small banks were strained, large

banks consolidated, and small and risky traditional business

lending overall fell dramatically. Measures to stabilize the

financial sector were surely necessary, but a more adaptive and

responsive political system would have been able to monitor

unintended consequences and fix them; instead, they have been

left to fester.

If this institutional malaise were only a federal phenomenon it

might feel more tractable. However, everything from local

permitting and zoning rules to poorly crafted state

environmental impact assessments conspire to stop progress in

its tracks at every turn. From neighborhood associations to

state licensing boards, the U.S. economy is now replete with

institutional gatekeepers who, after securing their own

preserve, close the door to opportunity behind them. With

respect to building, this manifests itself in private litigation

to stop key infrastructure projects that might connect

low-income workers with job opportunities, and in vocal

community opposition to even the most modest attempts to densify

development patterns or build anything but single-family housing

in opportunity-rich neighborhoods. If such tactics do not

prevent projects from proceeding altogether, they dramatically

raise the costs, ensuring that the country accomplishes less

with the resources at its disposal.

The ensuing distortions are flabbergasting: the country’s most

successful metropolitan agglomeration, the San Francisco Bay

Area, has been shedding domestic migrants for years, unable to

build sufficient housing to feed what should be the country’s

most magnetic industry cluster and opportunity-rich job market.

Such cautionary tales barely scratch the surface of how deeply

the tyranny of NIMBYism has harmed workers and reduced economic

growth and dynamism. Researchers Chang-Tai Hsieh and Enrico

Moretti found that restrictive land-use regulations in our most

productive cities have exacted a truly staggering toll, reducing

wage growth and dragging GDP growth in American cities down by

36 percent over the past five decades.

There are analogues across economic and social life, from

finance to housing, in which arguably fair competition in one

period gave way to unfair competition in the next. Competitive,

contestable market conditions need to be continuously secured,

because the winner in one period has every incentive to use all

tools at his or her disposal to ensure they are the winner of

each subsequent period too. In the social realm, this behavior

can be seen in the “opportunity-hoarding” of the upper-middle

classes, as Richard Reeves puts it, where public policy at all

levels is coopted to reinforce the advantages of the affluent

and upper middle classes, distorting the meritocracy much like a

leading firm might rationally use its available means to distort

the market in its favor.

The public’s weapons for safeguarding competition in

markets–proactive and robust antitrust enforcement, competent

regulators, and insurgent entrepreneurs–are all flagging.

Antitrust enforcement actions have been minimal since the

mid-1990s, and enforcement agency appropriations have fallen for

a decade. As knowledge, technology, and business grow

increasingly more complex, regulators with limited resources and

capacity are at ever greater risk of capture by incumbent

interests. And a negative feedback loop may already be

preventing startups from entering new markets, further cementing

incumbent advantage and deterring future startup activity.

In the end, sclerosis and gatekeeping are detrimental because

they prevent people from accessing economic opportunity. They

raise the cost of building things–literally and figuratively–in

the United States, diminishing the pace of progress and

restricting how broadly the benefits of progress can spread.

Broad institutional shortcomings that make it hard to afford

housing, change careers, or build a business constrain the

opportunity sets within which individuals make economic

decisions. Institutional sclerosis obstructs the sort of

risk-taking that is the lifeblood of a dynamic economy.

02 How Workers Benefit from a Dynamic Economy

The simplest way to understand how workers directly and

indirectly benefit from a dynamic and changeful economy is to

examine dynamism’s essential role in:

creating jobs;

boosting wages; and

providing economic opportunities for less advantaged

workers.

Creating jobs

New firms power a healthy job market. The most successful young

firms in any given year are responsible for nearly all of the

economy’s lasting net job creation. From 1990 to 2006, new firms

created an average of 2.8 million jobs each and every year. That

figure fell by more than one-fifth to 2.3 million following the

Great Recession, after which it failed to recover. The impact

has been significant. Recent research from the OECD suggests

that a 20 percent decline in startups (essentially what the

United States has experienced with the Great Recession) reduces

total employment down the road by 0.7 percent after three years

and 0.5 percent after 14 years. In other words, the startup

shortfall coming out of the Great Recession translated into a

national deficit of well over half a million jobs by 2019.

Nearly all of the country’s net job

creation has come from

startup

businesses over the past

two decades

Net job creation (millions)

Firms age 0 (startups)

2

0

2000

2005

2010

2015

Ages 1-5

0

-2

Ages 6-15

0

-2

Ages 16+

2

0

-2

-4

All firms

4

2

0

2000

2005

2015

-2

-4

Source: U.S. Census Bureau’s Business Dynamics

Statistics

Nearly all of the country’s net job creation has

come

from

startup businesses over

the past two decades

Net job creation (millions)

Firms age 0 (startups)

2

0

2000

2005

2010

2015

Ages 1-5

0

-2

Ages 6-15

0

-2

Ages 16+

2

0

-2

-4

All firms

4

2

0

-2

-4

Source: U.S. Census Bureau’s Business Dynamics

Statistics

Nearly all of the country’s net job creation has

come from

startup businesses

over the past two decades

Net job creation (millions)

Firms age 0 (startups)

2

0

2000

2005

2010

2015

Ages 1-5

0

-

2

Ages 6-15

0

-

2

Ages 16+

2

0

-

2

-

4

All firms

4

2

0

-

2

-

4

Source: U.S. Census Bureau’s Business Dynamics

Statistics

For all the pain that they cause, recessions can perform a

salutary function in the economy at large. Firms generally shed

their least productive workers in a downturn, and downturns are

usually hardest on the least productive firms. This creates an

opportunity for new, fast-growing, and more productive firms to

expand on the other side, offering laid-off workers better

matches and better wages to fuel an even stronger bounce back.

Tellingly, the Great Recession had less of a “cleansing” effect

on the economy than past recessions (meaning the rate at which

workers were reallocated from less productive to more productive

firms was far lower), in large part because new firm creation

rates were so weak in its aftermath. Steven Davis and John

Haltiwanger show this weakness was at least partly due to the

fact that the Great Recession was precipitated by a dual housing

and financial crisis, affecting both household equity and credit

markets—two essential sources of startup capital—severely. All

the same, one of the reasons the employment recovery from the

Great Recession took so long was because fewer startups were

there to help productively reabsorb the workers hit hardest by

the downturn. As a rule, established firms just do not grow

quickly enough during expansions to pick up all of the slack

they shed during downturns.

Boosting wages

Workers benefit when there is strong competition for their

labor. Yet, as high-growth young firms disappear and older

incumbents loom more dominant in labor markets, that beneficial

competition has weakened substantially. Ioana Marinescu

estimates that over 60 percent of local labor markets in the

United States are highly concentrated, covering one-fifth of the

U.S. workforce. Fewer employers means fewer potential buyers of

an individual’s labor and greater likelihood that a worker must

simply accept terms and wages set by whichever firm is hiring.

This imbalance not only translates into less job-to-job

mobility, but also into worse wage growth.

More competition among firms, by contrast, gives workers

leverage. With competing offers in hand and better alternatives

a click away, workers have more choice and power, and thus can

often bargain for higher pay. Nowhere is this more apparent than

in a comparison of wage growth rates for people who switch jobs

versus those who stay in their current jobs. Job switches are

strongly correlated with wage growth, both for the individual

and the broader economy.

Job switchers

consistently enjoy

higher wage growth than

other workers

Median wage growth

6%

4%

2%

Recession

periods

0%

2000

2004

2008

2012

2016

2020

Source: Federal Reserve Bank of Atlanta’s

Wage Growth Tracker

Job switchers

consistently enjoy higher wage

growth than other workers

Median wage growth

6%

4%

2%

Recession

periods

0%

2000

2004

2008

2012

2016

2020

Source: Federal Reserve Bank of Atlanta’s Wage

Growth Tracker

Job switchers

consistently enjoy higher wage

growth than other workers

Median wage growth

6%

4%

2%

Recession

periods

0%

2000

2004

2008

2012

2016

2020

Source: Federal Reserve Bank of Atlanta’s Wage

Growth Tracker

Even in the labor market, the role of startups as catalysts in a

dynamic system is critically important. The formation of new

firms and their subsequent hiring activity triggers job switches

that cascade through the labor market. These switches help

improve the quality of employer-employee matches. And as

discussed above, such labor market dynamism represents a broader

reallocation of the country’s workforce towards more productive,

faster-growing, higher-paying firms—an essential process for

sustaining the productivity growth that allows for living

standards to rise. Indeed, successful new startups generate much

of the country’s long-term productivity growth with their

innovations, which include new business models and new ways of

employing people. For individuals, job switching is a critical

method of accumulating human capital and associated with

stronger lifetime earnings.

Providing opportunities for less-advantaged workers

Robust startup rates and healthy labor market churn are

especially beneficial for workers with the weakest leverage in

the labor market,

particularly younger workers and those who have the lowest

levels of skill, wealth, social connections, or educational

attainment. Startups are disproportionately likely to hire young

people, immigrants, less-educated adults, and new labor market

entrants, for example. And Steve Davis and John Haltiwanger

calculate that when the workforce turnover rate (the sum of

total hires and separations over total employment) falls by 1

percentage point, the employment rate for men with less than a

high school diploma falls by 0.8 percentage points. It falls by

0.5 percentage points for equivalently-educated women (see

Figure 9). The situation is even worse for young workers in

their crucial early years in the labor market: for that same

decline of 1 percentage point in the worker turnover rate, the

employment rate for workers under the age of 25 with less than a

high school diploma declines by 1.4 percentage points for men

and 1.0 percentage point for women. Thus, less churn in the

labor market leads to less employment for those with the most

tenuous attachment to it. The slow recovery in turnover

following the Great Recession therefore seems correlated with

the slow jobs recovery experienced by so many segments of the

labor force (it took 13 years to recover all jobs lost in the

Great Recession, and not until 2019 did labor market turnover

recover to 2006 levels).

Less churn in the labor market

makes it harder for

jobseekers with

less education or work

experience

to find jobs

Change in employment from a 1 percentage

point decline in the worker turnover rate

Men

Women

Bachelor's

degree or more

-0.36%

-0.17%

Some college

-0.39%

-0.41%

High school

diploma

-0.61%

-0.16%

Less than a high

school diploma

-0.77%

-0.47%

Source: Davis and Haltiwanger. Working Paper 20479,

National Bureau of Economic Research, 2014

Less churn in the labor market makes it harder

for jobseekers with less

education or

work experience to find jobs

Change in employment from a 1 percentage point

decline in the worker turnover rate

Men

Women

Bachelor's

degree or more

-0.36%

-0.17%

-0.39%

Some college

-0.41%

High school

diploma

-0.61%

-0.16%

Less than a high

school diploma

-0.77%

-0.47%

Source: Davis and Haltiwanger. Working Paper 20479,

National Bureau of Economic Research, 2014

Less churn in the labor market makes it harder for

jobseekers with less education or work experience to find jobs

Change in employment from a 1 percentage point decline

in the worker turnover rate

Men

Women

Bachelor's

degree or more

-0.36%

-0.17%

-0.39%

-0.41%

Some college

High school

diploma

-0.61%

-0.16%

Less than a high

school diploma

-0.77%

-0.47%

Source: Davis and Haltiwanger. Working Paper 20479,

National Bureau of Economic Research, 2014

Job churn and opportunity go hand in hand because flux creates

more frequent job openings, allowing relatively disadvantaged

workers to get a foot on the first rung of a career ladder.

Labor market fluidity thus provides chances to limit spells of

unemployment, accrue critical on-the-job human capital, and seek

out progressively better job matches with higher wages.

Startups, meanwhile, tend to operate outside of the box and may

intentionally set out to hire from varied backgrounds. They

offer employment opportunities for individuals with greater risk

tolerances or particular ambitions and preferences that allow

for more non-standard matches to be made. In a less dynamic

labor market with fewer matches and fewer disruptive new

employers coming on the scene, workers from weaker positions or

untraditional backgrounds have a much harder time competing

successfully against those with stronger credentials, more

conventional career histories, or better connections. In other

words, a dynamic labor market in which new firms apply pressure

to incumbents and all firms are forced to compete harder for

labor helps those who are traditionally disadvantaged or

overlooked.

The symbiosis at the heart of creative destruction

Few events are as traumatic for a worker as losing a job when

their employer goes belly up. Yet the closing of unproductive

enterprises and the recycling of their assets into new and

better vocations is central to the healthy functioning of a

market economy–and to the longer-term well-being of workers

themselves.

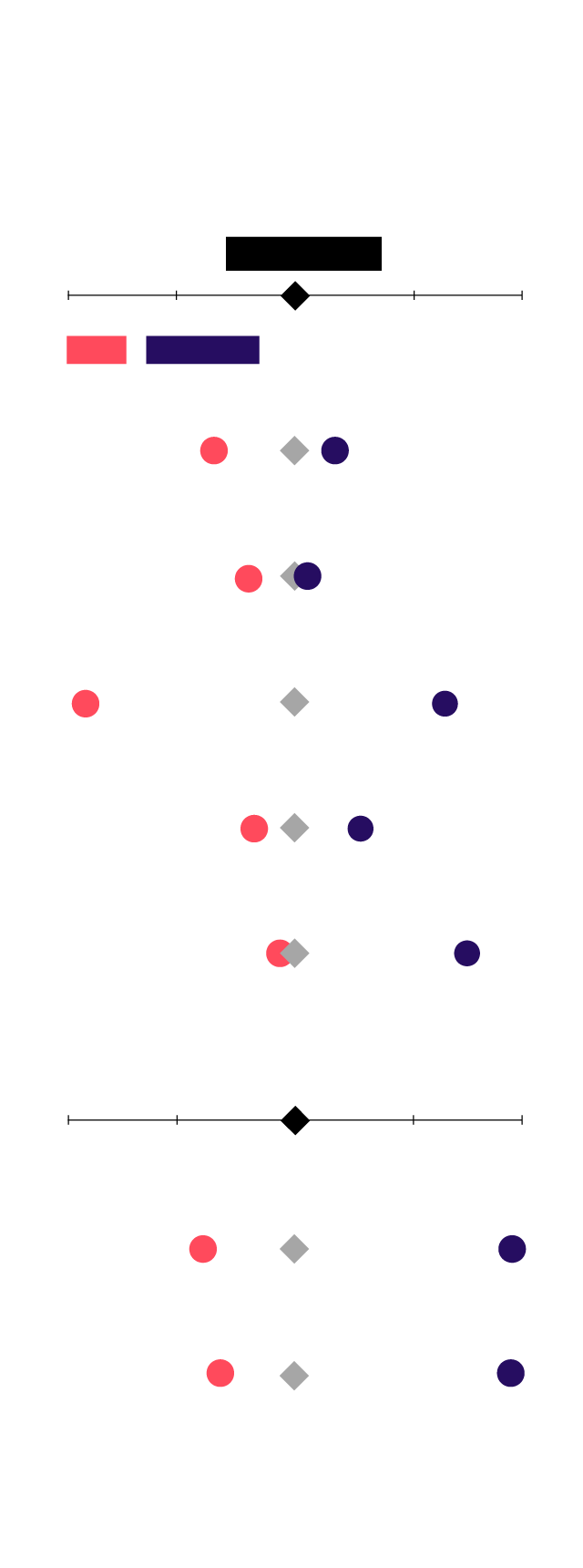

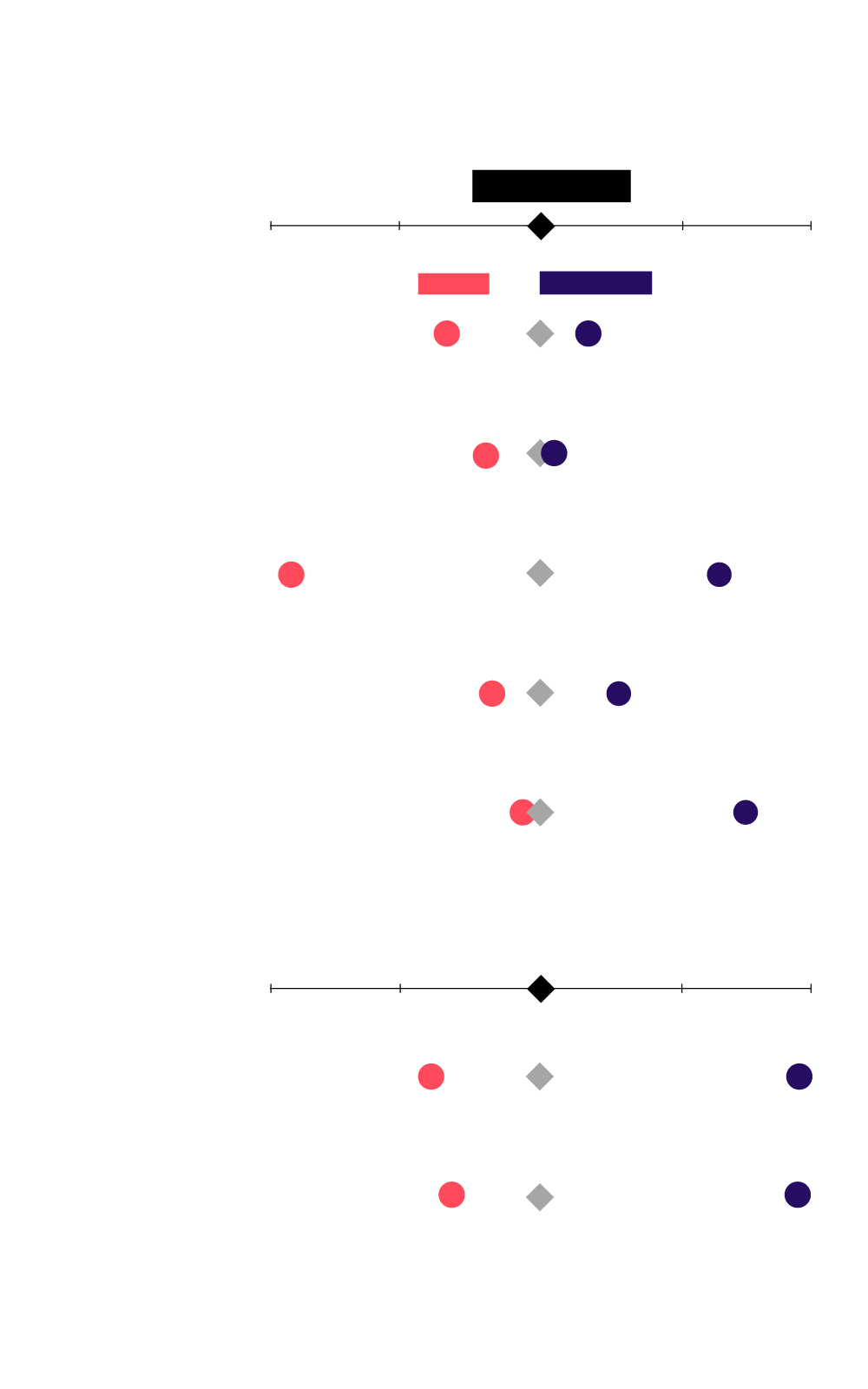

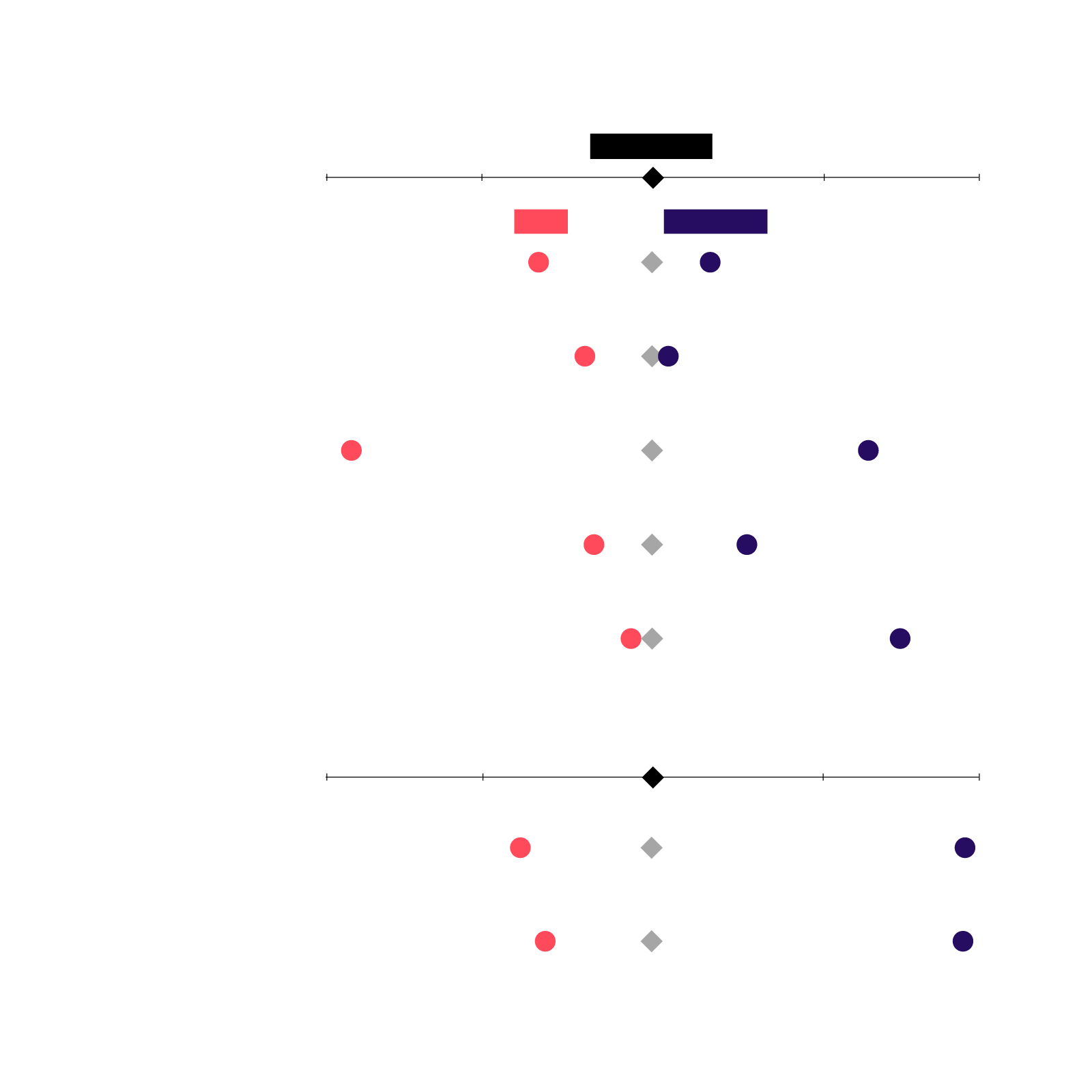

Colorado shows the power of a high-churn, dynamic economy in

action. The state has a firm death rate averaging 8.4 percent

in recent years–higher than the 8.1 percent average national

rate. Yet its startup rate averaged 9.3 percent, higher than

the national startup rate and easily eclipsing the statewide

rate of firm closure. In fact, states with elevated firm death

rates tend to have even higher startup rates, underscoring how

creation and destruction intertwine to fuel business dynamism.

And what does higher firm-level churn mean for a state’s

workers? From prime age employment rates to wages at all tiers

of the distribution, Colorado outperforms the nation in terms

of worker well-being and the abundance of economic

opportunity.

Halfway across the country, Ohio demonstrates the false

promise of an economic “stability” premised on low rates of

churn and change. Only 6.9 percent of Ohio’s firms closed in

the average year leading up to the pandemic, well below the

national rate. Yet the intensity of renewal was even lower;

the state’s 6.0 percent startup rate over the past three years

was one of the lowest in the country. Fully fourth-fifths of

the state’s workforce enjoys the assumed security of working

for an old, established firm, but prime age employment is low,

and wages lag at all points in the distribution. Ohio–like all

of its peers across the Eastern Heartland–is already farther

down the slope of diminished dynamism than the country as a

whole, and its workers are worse off as a result. In the

country’s lagging regions, stasis is the problem. To break out

of it, the velocity of creative destruction needs to be

rekindled.

Dynamic economies

outperform

static ones across

measures

of opportunity

Difference to national average in %

National Avg.

−6%

−3%

+3%

+6%

Ohio

Colorado

Average startup rate 2017-2019

6.0%

9.3%

8.2%

Average firm death rate 2017-2019

6.9%

8.4%

8.1%

Share of workers in younger firms

19.4%

29.2%

25.1%

Job reallocation rate

19.2%

22.1%

20.3%

Prime age employment rate

79.2%

84.3%

79.6%

Difference to national average in $

−2$

−1$

+$1

+$2

Wages (25th percentile)

$12.1

$14.9

$12.9

Wages (50th percentile)

$18.7

$21.3

$19.4

Source: U.S. Census Bureau’s Business Dynamics

Statistics, 2019; U.S. Census Bureau’s Current

Population Survey, 2018

Dynamic economies

outperform static ones

across measures of opportunity

National Avg.

−6%

−3%

+3%

+6%

Difference

to national

average in %

Colorado

Ohio

Average startup

rate 2017-2019

6.0%

9.3%

8.2%

Average firm death

rate 2017-2019

6.9%

8.4%

8.1%

Share of workers in

younger firms

19.4%

29.2%

25.1%

Job reallocation

rate

19.2%

22.1%

20.3%

Prime age

employment rate

79.2%

84.3%

79.6%

Difference

to national

average in $

−2$

−1$

+$1

+$2

Wages

25th percentile

$12.1

$14.9

$12.9

Wages

50th percentile

$18.7

$21.3

$19.4

Source: U.S. Census Bureau’s Business Dynamics

Statistics, 2019;

U.S. Census Bureau’s Current Population Survey,

2018

Dynamic economies

outperform

static ones across

measures of opportunity

National Avg.

Difference to national

average in %

−6%

−3%

+3%

+6%

Ohio

Colorado

Average startup

rate 2017-2019

6.1%

9.3%

8.2%

Average firm death

rate 2017-2019

6.9%

8.4%

8.1%

Share of workers in

younger firms

19.4%

29.2%

25.1%

Job reallocation

rate

19.2%

22.1%

20.3%

Prime age

employment rate

79.2%

84.3%

79.6%

Difference to national

average in $

−2$

−1$

+$1

+$2

Wages

25th percentile

$12.1

$14.9

$12.9

Wages

50th percentile

$18.7

$21.3

$19.4

Source: U.S. Census Bureau’s Business Dynamics

Statistics, 2019; U.S. Census Bureau’s Current

Population Survey, 2018

03 The Path to Renewal

As the country emerges from the COVID-19 pandemic, policymakers

confront a high-stakes opportunity to restore U.S. economic

dynamism and forge a more optimistic, aspirational future for

American workers. We believe such an agenda should start with

three fundamental policy goals that would deliver large and

pervasive benefits for all Americans:

First, dismantle federal- and state-level barriers to

competition and mobility in the labor market so that workers

can access the jobs they want, in the places they choose, at

the wages they deserve.

Second, embrace our national advantage as a magnet for

skilled immigration to fuel entrepreneurship and innovation,

boost demand for American workers, and support the revival

of struggling regions.

Third, end the tyranny of NIMBYism to make it easier,

faster, and more cost-efficient to build housing and

infrastructure so that America’s built environment can

accelerate, rather than stifle, economic adaptation and

resiliency.

While the political challenges of achieving these goals are not

insignificant, their budgetary impacts would be. At a time when

the sticker shock of federal spending has itself become a major

barrier to legislative progress, the U.S. can nevertheless reap

massive economic rewards from extremely low-cost policy

initiatives. Let’s look at each in turn.

Dismantle barriers to competition, mobility, and knowledge

diffusion in the labor market

Entrenched interests, usually in the form of incumbent

businesses, industries, and professional licensing and lobbying

associations have succeeded at steadily reducing the forces of

competition that benefit American workers. Gatekeeping

incumbents have used law and regulation to restrict how and

where workers can deploy their talents in the labor market,

while policymakers have largely been asleep at the wheel. In

fact, we’ve come to accept interference in the basic competitive

functions of the labor market as a normal part of life, rather

than a sometimes necessary exception. And workers have paid the

price. A dynamism agenda should start with aggressively rooting

out barriers that limit Americans’ ability to take risks, build

businesses, switch jobs, or move to different parts of the

country.

Nothing better sums up the creeping shift away from dynamism

than the proliferation of non-compete agreements. Non-competes

prohibit workers from fully exercising their freedom to switch

jobs for better opportunities or to use their work experience to

start a new business. A worker subject to such an agreement

signs a contract preventing them from becoming or working for a

“competitor” to their former employer in the near future, often

even if they are laid off or fired. Practically, non-competes

block workers from being poached for higher pay, jumping to a

peer company for better benefits or working conditions, spinning

out to create their own new and related enterprise, or even

deploying their talents in a new high-growth startup that could

become their community’s next major anchor employer. The

academic literature finds negative effects of non-competes

across the board, from stifling entrepreneurship and blunting

competition in product markets to suppressing worker wages and

reducing the survival rate of young firms. Economists including

Michael Lipsitz and Evan Starr have also found immediate worker

benefits in states that have curtailed their use.

Non-compete agreements are anathema to the basic principles of a

free and fair market, yet they have proliferated rapidly:

Low-end estimates suggest they cover nearly one-fifth of all

U.S. workers, including millions of low-wage workers in

industries such as fast food restaurants, custodial services,

and transportation. They are often quite difficult for workers

to challenge in legal settings. As a result, non-competes trap

millions of workers in their current jobs. Fortunately,

progressive and conservative reformers alike have taken notice.

For example, the bipartisan Workforce Mobility Act currently

before Congress would ban the use of these agreements nationwide

under most circumstances. Not waiting for Congress to act, many

states are taking meaningful steps to curtail the use and abuse

of non-competes: fully half of all states considered

non-competes reform in 2021 alone.

Just as non-competes give employers the means to limit

competition for their workers, onerous occupational licensing

requirements enable incumbent businesses to erect barriers to

competition within their industries. Seminal research by Morris

Kleiner demonstrates that licensing requirements applied to an

estimated 1 in 20 U.S. workers in 1950 but have since spread to

an estimated 29 percent of the workforce. Overly expansive

licensure has been shown to impose higher prices on consumers,

restrict the geographic mobility of licensed workers, raise the

costs associated with entering into certain professions, and

reduce the wages and economic opportunities of unlicensed

workers. These drawbacks have motivated bipartisan calls for

reform focused on rigorous cost-benefit analyses, uniform

standards and reciprocity across states, and outright

elimination of requirements for entry into certain professions.

The proliferation of non-competes and licensing requirements

have harmed U.S. dynamism in another way: reducing the spread of

knowledge and know-how throughout the economy. By making it more

difficult to switch to better jobs, start a better company, and

move to a better area, they weaken the invisible circulatory

system that distributes expertise and makes innovation and

productivity gains possible.

The exigencies of the pandemic have revealed the costs of such

labor market distortions. Millions of workers have gone

freelance and don’t want to go back to a traditional work

setting. States have suspended certain licensing requirements or

adopted reciprocity with other states specifically for

healthcare workers in order to fill critical skill gaps. The

worker shortage across the economy may make employers more

amenable to non-competes reform, too, as the cost of measures

that gum up the labor market make themselves felt more acutely.

Embrace our immigration advantage

Better immigration policy is one of the most powerful tools

available for boosting American dynamism. However, our current

immigration regime is ad hoc and poorly designed, and it fails

to place sufficient emphasis on maximizing the economic benefits

of immigration to the American economy and its workers. To boot,

the number of legal immigrants into the United States has

dropped severely in recent years due to policy shifts, pandemic

effects, and a bureaucracy crumbling under its own weight and

unable to process even simple visa renewals. The result was a

multi-decade low in net international migration in 2021, falling

three-quarters from over 1 million net newcomers in 2016 to

fewer than 250,000 in 2021.

The case for high-skilled immigration should be self-evident.

Skilled workers offer high local economic “multipliers,” given

their higher wages, meaning their economic contributions locally

and nationally are positive and outsized. Knowledge

workers—native and foreign-born alike—are complementary to each

other, and demand for knowledge workers is nearly unlimited in

today’s economy; the supply of them is the binding constraint on

economic growth. Thus, the conventional worries about

substitution or crowd-out with vulnerable native born workers

that plague political debates over immigration do not apply.

Instead, welcoming more highly skilled immigrants would help the

country perform at the frontiers of its potential.

Research by Pierre Azoulay and colleagues also shows that

immigrants’ propensity towards entrepreneurship means they play

a much more significant role as “job creators” than “job takers”

in the U.S. economy. Put immigrants’ many economic roles

together and their consumption, investment, and entrepreneurship

all help to boost demand for domestic labor, supporting native

employment and wages. Importantly, expanding the flow of

high-skilled immigration would yield powerful benefits

throughout our economy quickly and at extremely low cost.

It is difficult to overstate how badly today’s U.S. immigration

policy falls short of its potential. This country is unique in

its status as the overwhelmingly preferred destination of

would-be migrants across the world. As such, simply by enacting

sensible policies, we can enjoy the presumption of practically

limitless access to scientists, engineers, medical

professionals, and other in-demand talent the world over. This

attractiveness to talent is arguably the single greatest

advantage any nation can possess. But instead of embracing it,

we continue to languish in an incoherent and self-defeating

approach that fails to identify the right goals or facilitate

the best outcomes. We must do better.

Pro-dynamism immigration reform should start by improving

existing pathways like the H-1B visa so that they are easier to

administer, decoupled from a single employer, and more readily

accessible to new, small, and medium-sized enterprises. But

improving existing pathways is only the beginning. The United

States needs new pathways for skilled immigrants that are linked

to specific goals, namely: increasing entrepreneurship, boosting

STEM talent in the workforce, and bolstering the economic

well-being of lagging regions. And rather than caps, our skilled

immigration policy should be oriented around aggressive targets

for welcoming the world’s most talented and hard-working people.

Perhaps the most obvious way to expand high-skilled immigration

is by creating a startup visa for immigrant entrepreneurs. Such

a program would create a special fast-track for those with

promising ideas, proven fundraising ability, and the desire to

build their businesses in the United States and create jobs for

native-born Americans. Immigrants already contribute in profound

ways to American entrepreneurship. On average, immigrants are

significantly more likely to start a business than native-born

Americans, and they are responsible for founding a large share

of today’s biggest and most successful companies. The global

competition for entrepreneurial talent will only grow fiercer in

the coming decades. Establishing a startup visa is an excellent

way to help ensure that the short-run boom in pandemic-era

startups leads to a lasting and widely beneficial revival in

American entrepreneurship.

The United States should also employ immigration as a regional

economic development tool. For example, a place-based “heartland

visa” would provide benefits and incentives to skilled

immigrants who settle in parts of the country contending with

economic stagnation and the loss of prime age workers. The

economic impact would go beyond supplying needed skills to local

businesses. Newcomers would bolster housing markets, supporting

the wealth of local residents. They would fortify municipal tax

bases, thereby improving services for native families. Their

presence would improve local economic prospects, drawing new

businesses and employers to places struggling with attrition.

And since immigrants have a high propensity for

entrepreneurship, heartland visas would recruit people

disproportionately likely to start businesses and drive growth

in the future to areas that have been left behind. While

immigrants have long played these important roles in legacy

cities, national immigration policy itself hasn’t been designed

with the needs of such communities in mind. It’s time for that

to change.

Boosting immigration would also help address one of the major

forces behind the decline of U.S. dynamism: rapid demographic

decline. Indeed, the precipitous drops in fertility and

population growth now underway in the United States represent an

unprecedented challenge for policymakers. Never before has this

country had to confront the reality of sustained demographic

decline or a shrinking prime-age workforce. America may never

again achieve the demographic vitality that characterized the

20th century, but we need not accept the dire consequences of

demographic collapse.

Build, baby, build!

The built environment must be adaptable for the economy to

evolve. Local housing supplies must be elastic enough to ensure

that hubs of innovation can also serve as destinations for

workers seeking better opportunities. Cleaner technologies must

be both manufactured and deployed in order to decarbonize the

economy. Productivity-enhancing infrastructure investments must

be realized to deliver social and economic dividends. But on all

of these fronts, the United States has become mired in a costly

artificial paralysis that has turned our nation’s built

environment into a hostage of interests deeply opposed to its

continued development.

The practical inability to build so many things across so much

of the country is an almost entirely self-inflicted wound and

serves as a hefty tax on American dynamism. We’ve allowed

pervasive, supply-constraining regulations to disfigure the

housing market—and then are puzzled over why housing is so

scarce and expensive in places where demand is the highest.

We’ve allowed poorly designed policy and regulatory complexity

to make efficient infrastructure spending impossible—and then

wondered why our basic infrastructure is the most expensive to

build of anywhere in the developed world. We hear countless

exhortations about the threat of climate change–then watch as

the necessary process of transitioning to a cleaner energy

economy get stymied in the purgatory of permitting hurdles and

community-level vetoes.

Simply put: NIMBYism has become nothing short of a monumental

threat to progress and prosperity.

Aggressive local, state, and federal leadership will be required

to pull the country out of the morass of regulatory barriers and

stakeholder vetoes that prevent the foundation of the future

from even being laid. A handful of localities across the country

have begun the slow process of reforming local land-use and

zoning codes in recognition of how exclusionary practices have

driven up housing prices, fueled inequality, and undermined

economic prospects and wealth accumulation for low-income

families. More states should follow the lead of Massachusetts,

for example, which signed into law in January 2021 a requirement

that municipalities allow for multi-family real estate

development around transit stations. The core goal for reformers

should be simple: allow more of the U.S. housing market to

function as an actual market—one in which demand can efficiently

be met with supply, and special interests are not empowered to

block progress at every turn.

States and the federal government should fully leverage the

power of the purse to incentivize state and local land-use

reform. Our federalist system grants localities considerable

rights around land use, but that does not mean the federal

government must remain agnostic about local planning decisions

and subsidize regressive practices with far-reaching negative

externalities. Instead, eligibility for key funding streams

around infrastructure and housing, to name a few, should be

predicated on a minimum level of land use liberalization and

procedural efficiency. Places that implement best practices

should be rewarded accordingly. And federal lawmakers need at

long last to tackle the massive policy-related inefficiencies

that plague federal infrastructure spending and dilute its

economic benefits. At the end of the day, how much is spent on

infrastructure–the question that still dominates political

discussions–only matters in relation to how efficiently that

money is actually spent.

These three pillars are of course only the beginning of a fully

formed dynamism agenda. We also need greater and more effective

federal investment in basic research and development, for

example, as well as a modernized approach to innovation policy.

We need a social safety net that encourages the kinds of healthy

risk-taking that is essential to a mobile and entrepreneurial

society. We must do better at retraining workers and helping

them rebound from economic shocks. We should examine how our

system of intellectual property protections can be improved to

balance tradeoffs and prevent abuses that work against the

public interest. And drawing from the lessons of the tepid

recovery from the Great Recession, we need a macroeconomic

policy environment that pushes the labor market to operate at

full employment, with all the attendant benefits it achieves for

American workers.

At its heart, the task is to improve the economy’s circulatory

system so that it can naturally deliver better outcomes for

workers, families, and communities, thereby limiting the scale

and cost of other interventions.

Conclusion

Working Americans have far more to lose from an economy that is

changing too little and too slowly than from one that is quickly

adapting and advancing to new frontiers. To see that this is

true, we need only look back to our not-too-distant past, when

standards of living were booming alongside rates of mobility,

job switching, population growth, and startup activity that make

those of the 21st century seem anemic by comparison.

But in recent decades, policymakers have ignored signs that the

dynamic mechanisms at the heart of our economy were growing

weaker. Worse still, policy failures at every level of

government have contributed to the sclerosis that has slowly

robbed the country of its vitality. From NIMBYs to non-competes,

vested interests have steadily weighed the economy down with

artificial barriers to mobility, competition, and adaptation.

These barriers have made our economy less abundant in

opportunity and less able to improve the lives of ordinary

Americans.

There are many reasons to be hopeful in spite of the challenges.

The United States remains an enormously prosperous and capable

country—one with unique cultural and economic advantages, such

as our historic openness to change, our embrace of pluralism,

and a deep-seated, ambitious brand of optimism. The speed and

resiliency with which the U.S. economy adapted to the

coronavirus pandemic are proof that the country’s dynamism may

have subsided, but its embers can be rekindled. Now,

policymakers must seize the opportunity to turn temporary gains

into something sustainable, securing a dynamic and prosperous

future for generations of American workers to come.