by Kenan Fikri

It was too good to last. At the height of a global pandemic, Americans became more confident than ever that they would be able to retire comfortably. This peace of mind was delivered by federal fiscal support to households and a financial market bonanza fueled by unprecedented monetary stimulus. And it took hold towards the tail end of a nearly uninterrupted rise in asset prices made possible by the low-interest rate monetary policy environment since 2009.

Alas, the latest results from the University of Michigan's Survey of Consumers show that Americans' expectations for a comfortable retirement have fallen back to earth. New data show that retirement security sentiment now stands well below pre-pandemic levels, officially ending the long bull-run hopeful retirees enjoyed working towards for most of the prior decade.

The survey asks two questions especially pertinent to the country's current retirement security debates that together offer real-time insight into Americans' confidence in their long-term financial well-being:

- Change in likelihood of a comfortable retirement: "Compared with 5 years ago, do you think the chances that you (and your husband/wife) will have a comfortable retirement have gone up, gone down, or remained about the same?"

- Chances of adequate retirement income: "What do you think the chances are that when you retire, your income from Social Security and job pensions will be adequate to maintain your living standards?"

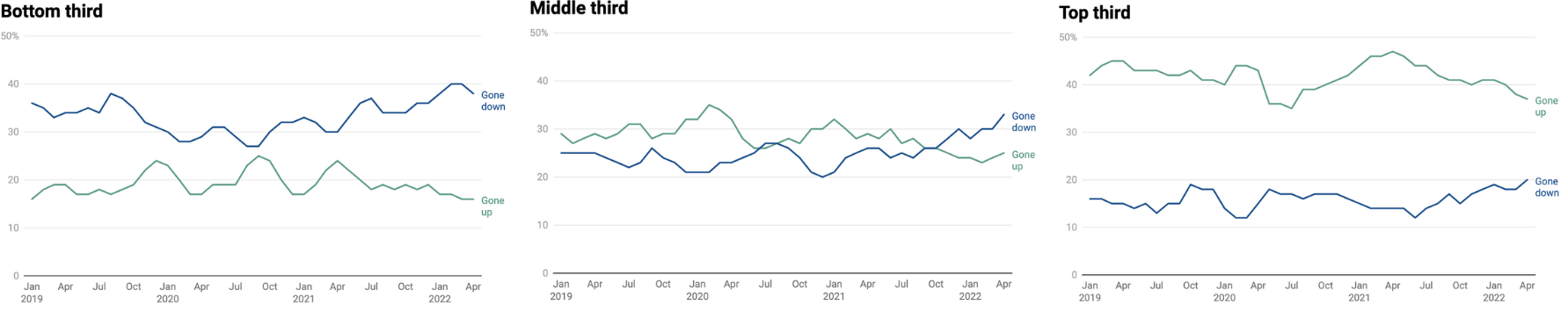

More Americans feel their retirement prospects are ebbing

Since December 2021, the share of respondents who believe that their chances of a comfortable retirement have gone down relative to five years ago has again exceeded the share who think that those chances have gone up. This marks an end to a decades-long run of gradually improving retirement expectations coming out of the exceptional pessimism wrought by the 2008 financial crisis. It took Americans several years to start feeling optimistic about their retirement prospects again in the wake of that traumatic event, which had a devastating impact on retirement portfolios. More recently, sentiment has started to drift back down after peaking in mid-2020, now approaching levels last seen around 2017 with a good chance that expectations deteriorate further. The decline in sentiment coincides with the acceleration in inflation and the related, growing uncertainty in financial markets.

Lower- and middle-income Americans are feeling the reversal most acutely

Sentiment has worsened substantially more for respondents in the bottom two-thirds of the survey's income distribution than for those in the top one-third. The share reporting that their chances of a comfortable retirement have gone down has risen by 11 percentage points for those in the bottom one-third and by 13 percentage points for those in the middle one-third relative to their pandemic-era lows. One-third of middle class respondents now see their chances of a comfortable retirement waning, compared to one-fifth in late 2020. Since October 2021, middle-class respondents with negative outlooks outnumber those with positive outlooks, marking an end to the era in which brighter outlooks dominated.

"Compared with 5 years ago, how do you think the chances that you will have a comfortable retirement have changed?"

The pandemic bump faded first and fastest for the lowest-income Americans

Retirement optimism has faded fastest for respondents in the bottom one-third of the survey's income distribution. This is most evident in the results from the second question, which asks about the overall chances of having an adequate income at all in retirement, not just the changes in those chances.

The probability that the typical respondent in the bottom one-third believes they will have a retirement income sufficient to maintain their current standard of living has fallen 5.8 percentage points since peaking in 2020, more than twice as fast as the 2.3 percent decline for respondents in the top one-third. The federal fiscal response to the pandemic buoyed sentiment most strongly for the middle group, for whom chances of a comfortable retirement remained elevated through late 2020 before falling swiftly thereafter. Retirement optimism is now below January 2020 levels for both of the bottom two thirds.

The expectations for the top one-third have proven more resilient, however. Even after retreating slightly over the past two years, the top one-third of respondents are more confident than ever in the pre-pandemic history of the survey that they will maintain their (by definition, already higher) living standards in retirement–attributable to the historic and extraordinary gains Americans with asset holdings have enjoyed over the past several years.

Why are Americans–especially lower and middle income ones–growing more pessimistic about their retirement prospects? Several factors are likely at work. First, the specter of inflation looms largest for savers, and those who have put together a modest nest egg for their retirement may worry that its long-term value is being eroded. A natural rebalancing from the pandemic's financial excesses may also be at work: household savings skyrocketed in 2020 as Americans dramatically curtailed spending outside the home and generous stimulus checks topped up savings accounts further. Being more flush with cash than usual gave American households a new sense of wealth and financial security. Now, that wealth effect is fading as households draw down their savings and habits normalize. The pandemic provided a one-time confidence boost that has now passed.

The pandemic's lasting dividends?

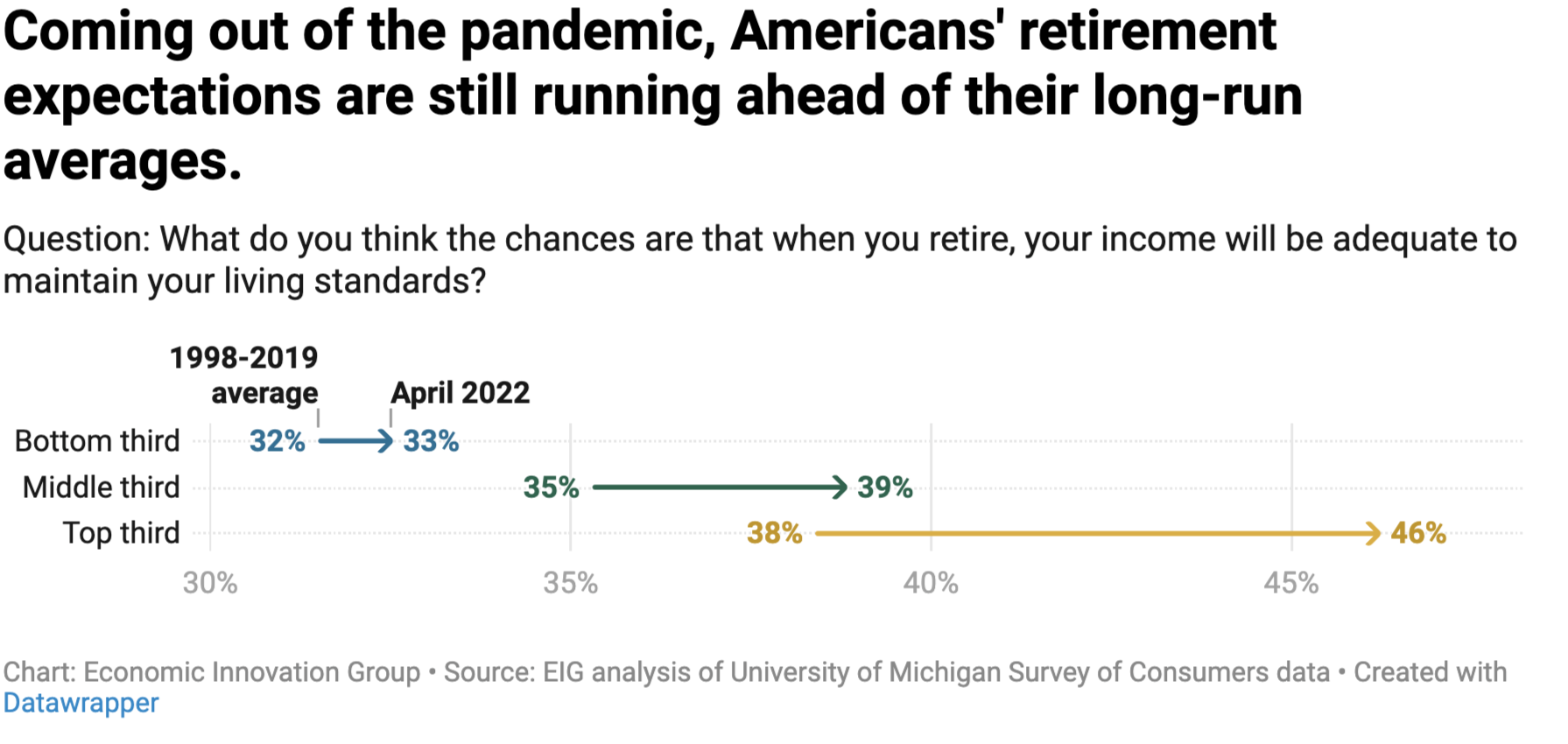

Yet the pandemic may still have a lasting and modestly positive effect on Americans' household finances. Another way to look at the figures is to compare current sentiment to long-run averages. This makes clear that, even amid surging inflation, strong household balance sheets coming out of the pandemic combined with a red-hot labor market have helped bolster retirement expectations for all brackets. This exceptional point is worth resting on: the deepest, sharpest recession in generations did very little harm to household finances; a swift federal response actually meant that most Americans came out ahead. Sentiment may now be turning down, but it remains very strong. Even lower-income Americans feel more confident in their retirement incomes today than they have on average since 1998.

Nevertheless, large inequalities persist. The bottom one-third of earners only outpace their long-term average chances of a comfortable retirement by 1 percentage point, compared to 7.8 percentage points for the top. The pandemic did nothing to close the relative retirement security gap between high-earners and low ones—instead, it widened it.

More avenues to asset ownership and accumulation for low- and middle-income brackets would help fortify retirement incomes and expectations for the bottom two-thirds of earners. A counterfactual economy in which they had been able to derive similar benefits–even proportional to their lower incomes–from the long-run increase in asset prices experienced since 2009 would have been powerfully more equitable. Markets fluctuate, as any reader watching their portfolios recently can attest, but over the long-term, they offer strong, reliable returns–and with that, greater financial security for Americans once they retire. More active and extensive participation in financial markets likely explains the greater confidence the top one-third of earners can express in their retirement prospects, despite economic headwinds. Lower-earning adults should be able to enjoy similar peace of mind.

Novel avenues to encourage long-term investing among lower-earning workers would help. The recent announcement of a bipartisan, bicameral Congressional working group focused on expanding high-quality savings vehicles and bolstering retirement security is a promising development. Leaders across the country agree, as evidenced by the US Conference of Mayors–whose membership includes over 1,400 mayors from across the nation–overwhelming passage of a resolution encouraging Congress to look to the highly successful Thrift Savings Plan (TSP) as a model for expanding savings opportunities for workers left behind by the current system. Installing more broad-based and inclusive opportunities for wealth-building at the national scale was one of the greatest missed opportunities of the post-recession era. Federal lawmakers now have a chance to ensure more Americans can harness the country's next economic upswing for their own retirement security.