Inclusive Wealth Building Initiative

How to Build Wealth, Reward Work, and Boost Well-Being for Millions of American Workers

The U.S. economy is the world’s most powerful engine for wealth creation. However, far too few Americans have a direct stake in the rewards of national economic growth and prosperity.

In a new white paper co-authored by a bipartisan pair of economists, Professor Teresa Ghilarducci, a labor economist at the New School and leading expert on retirement security, and Dr. Kevin Hassett, Vice President and Managing Director of The Lindsey Group and the former Chair of the White House Council of Economic Advisers, explore the potential of helping working Americans build wealth and retirement security through a long-term savings program modeled after the federal Thrift Savings Plan (TSP).

Low- and moderate-income Americans need help building wealth

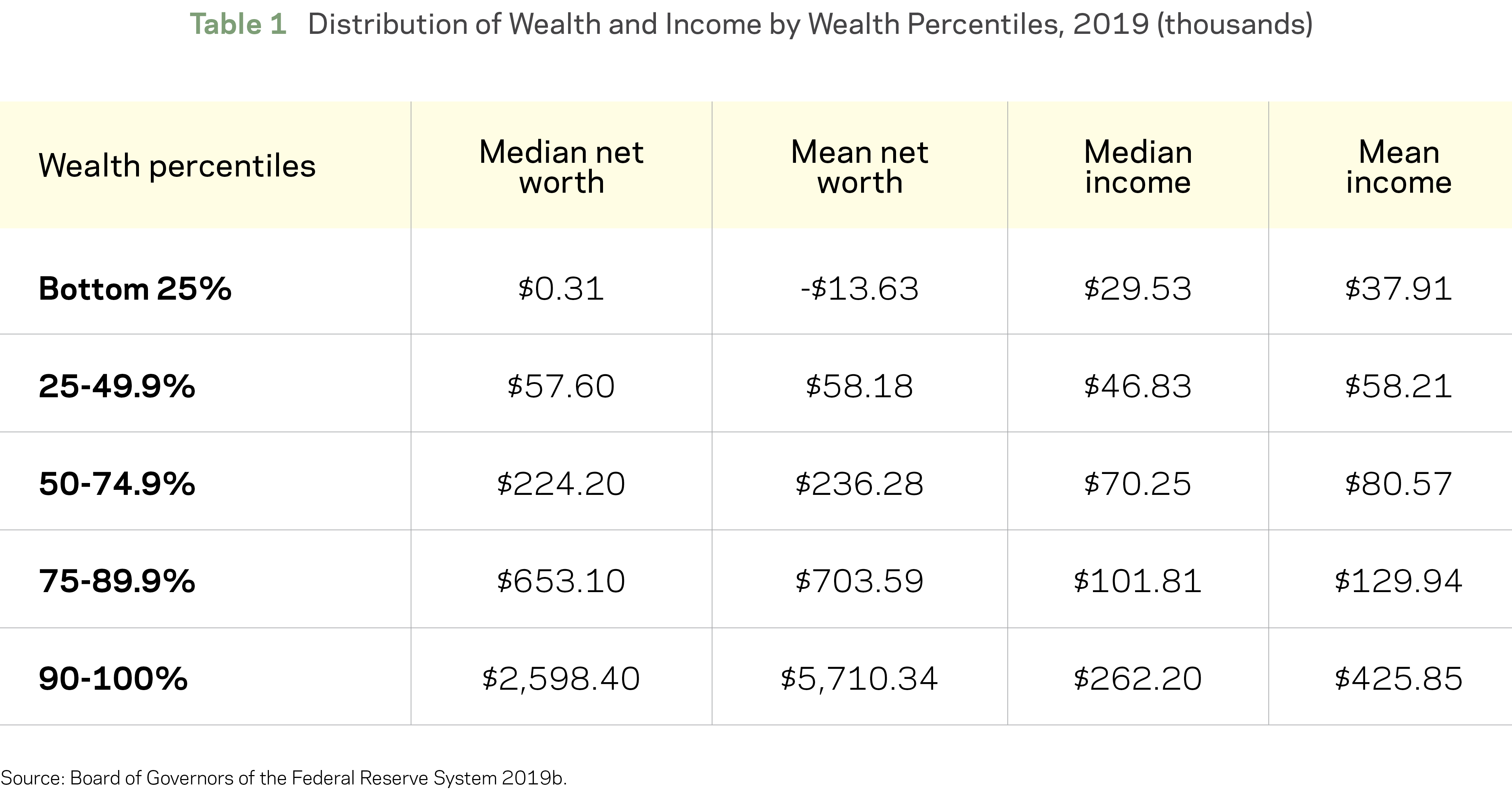

The lack of wealth for so many Americans is striking: The median net worth for the bottom 25 percent of American families is only $310. Moreover, World Inequality Database data shows the bottom 50 percent of American families own only 1.5 percent of total U.S. wealth. The uneven impact of the COVID-19 crisis threatens to repeat historical patterns in which the benefits of economic recovery bypass low- and moderate-income Americans. As we look beyond short-term relief in the months ahead, it is critical to address the longer-term challenge of ensuring a greater share of workers are able to build savings and achieve financial security.

Enabling working Americans to build retirement savings is critical to closing the wealth gap

The absence of retirement savings among a large share of American workers is a leading factor behind persistent wealth inequality. Troublingly, the median retirement savings balance for the bottom 50 percent of American families is $0. Estimates suggest that roughly one-half of workers do not participate in an employer-sponsored retirement plan (e.g., a 401(k) or pension). This lack of participation is particularly true for lower-income Americans: Workers in the top 25 percent of wages are more than twice as likely to have access to such a plan as low-income workers in the bottom 25 percent. Social Security can help prevent older Americans from falling into poverty, but it was never intended to fully support an individual’s entire retirement. The widespread lack of retirement savings also significantly disadvantages future generations, leaving low-income children responsible for the financial security of their parents and stunting their ability to save for their long-term needs. This cycle only solidifies the intergenerational nature of the wealth gap.

Enabling working Americans to build retirement savings is critical to closing the wealth gap

The absence of retirement savings among a large share of American workers is a leading factor behind persistent wealth inequality. Troublingly, the median retirement savings balance for the bottom 50 percent of American families is $0. Estimates suggest that roughly one-half of workers do not participate in an employer-sponsored retirement plan (e.g., a 401(k) or pension). This lack of participation is particularly true for lower-income Americans: Workers in the top 25 percent of wages are more than twice as likely to have access to such a plan as low-income workers in the bottom 25 percent. Social Security can help prevent older Americans from falling into poverty, but it was never intended to fully support an individual’s entire retirement. The widespread lack of retirement savings also significantly disadvantages future generations, leaving low-income children responsible for the financial security of their parents and stunting their ability to save for their long-term needs. This cycle only solidifies the intergenerational nature of the wealth gap.

Unfortunately, the current system simply wasn’t designed to maximize and reward participation among those most in need of building wealth. And the reason is simple: federal policy relies on tax deductions that overwhelmingly skew towards more affluent workers, and are useless to most low-income workers who pay little or no federal income tax to begin with.

In other words, those most in need of building wealth are implicitly excluded by current savings incentives.

The Thrift Savings Plan is a proven model for building wealth

To address this glaring gap in policy, Professor Ghilarducci and Dr. Hassett propose giving low- and moderate-income Americans access to a program modeled after the TSP, which is currently available only to federal employees and members of the military. This highly successful program features automatic enrollment for eligible workers, simple plan options, very low fee ratios, and matching government contributions. Research finds that the TSP performs particularly well for low-income and less educated workers–the very ones that have largely been left behind by U.S. retirement policy.

The new paper illustrates that making such a program broadly available to those who lack access to an employer-sponsored plan would dramatically improve the ability of lower-income workers to build assets over the course of their careers, thereby ensuring a more secure retirement and the chance to pass along wealth to future generations. And it could be achieved at relatively little cost to the federal government while protecting Social Security and avoiding new financial burdens on small businesses.